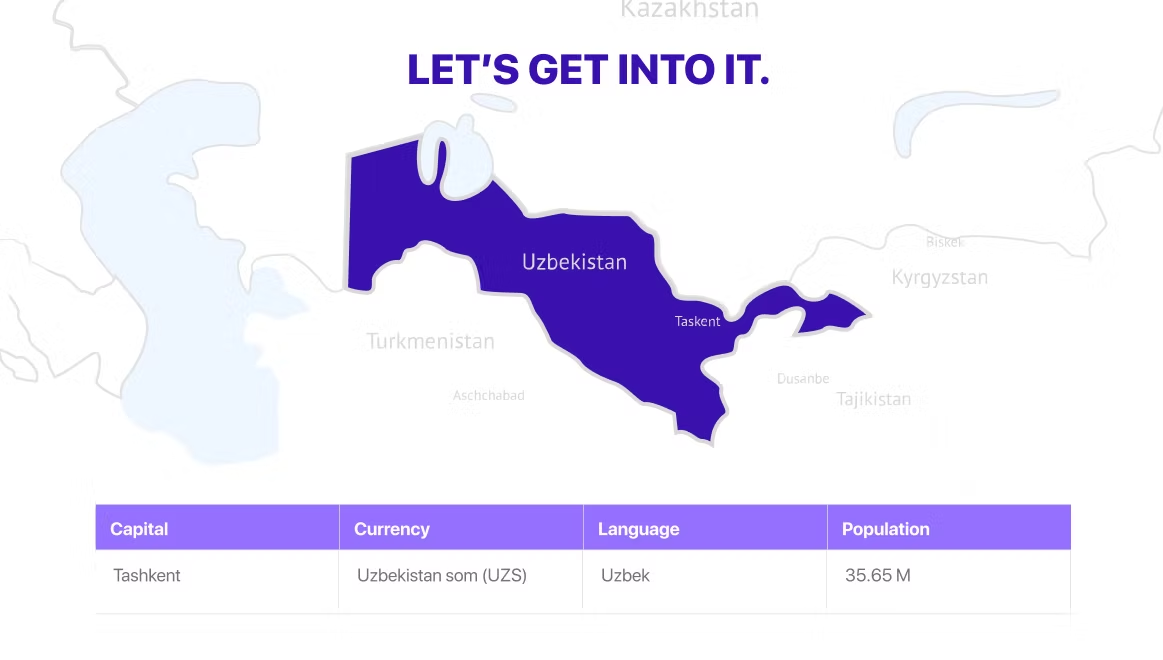

Relocation to Uzbekistan: Legal Requirements and Practical Steps

TL;DR

Central Asia is not what it was ten years ago.

And Uzbekistan is not what it was in 2016.

Since 2017, the country has shifted from a tightly controlled, state-centric economy to one that actively courts foreign capital, digital businesses, and regional headquarters. As we move toward 2026, that transformation is no longer cosmetic. It’s structural.

Two major legal developments, Presidential Decree No. UP-180 and Law No. ZRU-1101 has reshaped how residency, taxation, and labor compliance function for foreign individuals and companies. If you’re considering relocating talent or setting up regional operations in Uzbekistan, the rules have fundamentally changed.

This report focuses on three core pillars:

- How tax residency works under the new 2026 regime

- What incentives does T Park offer digital and tech businesses

- How Employer of Record services help companies operate compliantly without building a full local infrastructure

Quick Navigation

- TL;DR

- The Strategic Pivot. Uzbekistan’s Economic Liberalization (2017–2026)

- Residency by Investment and the Golden Visa Program

- The IT Park Ecosystem: Relocation Incentives for Tech Firms

- Employer of Record (EOR) vs. Entity Establishment

- Labor Compliance and the UNLS Framework (2026)

- Comprehensive Payroll and Taxation for 2026

- Social Insurance Law (ZRU-1101) and Employee Benefits

- Practical Relocation Steps: Logistics and Integration

- Comparison of Local EOR Providers for Relocating Companies

- Risk Mitigation: The "Gray Market" and Compliance Trends

- Conclusion: Uzbekistan as a Regional Hub in 2026

- Frequently Asked Questions

The Strategic Pivot. Uzbekistan’s Economic Liberalization (2017–2026)

To understand Uzbekistan today, you have to understand what it used to be.

Before 2017, the country operated under strict currency controls, limited foreign access, and an administrative-command system that discouraged outside investment.

The turning point came in 2017 with foreign exchange liberalization. That move unlocked broader reform. It signaled to investors that Uzbekistan intended to align with global standards, including WTO integration.

From 2017 onward, reforms accelerated:

- Foreign currency convertibility normalized

- Business registration digitized through Single Window systems

- International accounting standards adopted

- Local governments shifted toward performance-based management

By 2025–2026, the shift moved beyond liberalization into something more deliberate. Investor-centric governance.

The legal framework now flows from:

- The Constitution

- Constitutional laws

- Codes

- Ordinary laws

- Presidential decrees

Within that structure, Presidential Decree No. UP-180 stands out as a defining instrument for foreign individuals and executives considering Uzbekistan as a base.

The 2026 Special Tax Regime. A New Doctrine of Vital Interests

The traditional model for tax residency globally revolves around the 183-day rule. Spend more than half the year in a country, and you become a tax resident.

Uzbekistan has broken from that model.

Beginning January 1, 2026, foreign citizens may qualify for tax residency under a Special Tax Regime with only 30 calendar days of physical presence within a consecutive 12-month period.

Yes. Thirty.

But this is not a loophole. It is conditional.

The regime prioritizes the establishment of meaningful personal and economic ties over pure physical presence.

This framework is designed for:

- High-net-worth individuals

- Senior executives

- Board members

- International portfolio managers

In other words, people who operate across jurisdictions need a stable, compliant tax anchor in Central Asia.

Eligibility and the 30-Day Rule

Under the new doctrine, physical presence alone is no longer decisive. Instead, authorities evaluate whether the applicant has established substantive connections, often referred to as “vital interests.”

While implementation guidance continues to evolve, qualifying criteria generally include:

- Financial investment or economic activity in Uzbekistan

- Maintenance of local banking relationships

- Registered residential address

- Corporate governance or managerial involvement within Uzbek entities

The message is clear. Uzbekistan is not seeking tourists. It is seeking committed economic participants.

This reduced threshold dramatically enhances Uzbekistan’s positioning relative to other jurisdictions that still rely exclusively on the 183-day benchmark.

For internationally mobile executives, the flexibility is strategic.

Why This Matters

The geopolitical positioning of Uzbekistan is not accidental.

The country sits at the intersection of:

- Traditional Silk Road trade corridors

- Growing regional supply chains

- Expanding digital service ecosystems

It is actively repositioning itself as a regional headquarters hub for:

- Central Asia

- CIS markets

- Select Middle East and Eurasian corridors

With regulatory modernization underway and tax residency flexibility introduced, Uzbekistan is signaling long-term seriousness.

The Compliance Reality

Opportunity does not eliminate complexity.

Residency status, labor compliance, payroll reporting, and local tax administration remain structured and formal. Uzbekistan’s regulatory environment is improving, but it is not frictionless.

Companies relocating individuals or managing teams must navigate:

- Tax residency filings

- Employment law compliance

- Social contributions

- Local payroll administration

- Work permit and immigration rules

This is where many organizations underestimate the operational load.

| Requirement Category | Specific Criteria for Special Regime |

| Physical Presence | 30+ days in any consecutive 12-month period |

| Housing Anchor | Ownership of residential property or a long-term registered lease |

| Entrance Fee | One-time, non-refundable payment of USD 50,000 |

| Family Surcharge | USD 10,000 per adult family member |

| Infrastructure | Account in an authorized bank or a licensed crypto wallet |

| Reporting | Annual simplified notification format |

The establishment of a "legal anchor" through real estate is critical. If an applicant chooses to rent, the contract must be officially registered with the tax authorities—a measure designed to prevent the use of "fake addresses" or paper-only residences. This requirement, combined with the 30-day presence, allows the individual to claim Uzbekistan as their "center of vital interests," which is a key concept in avoiding double taxation under international treaties.

Fiscal Implications of the UP-180 Regime

The primary incentive of the special regime is the exemption of non-Uzbek-sourced income from local Personal Income Tax (PIT). While the standard PIT rate in Uzbekistan is a flat 12%, participants in the UP-180 regime are shielded from this tax on income earned outside the country.

| Income Source | Standard PIT Rate | UP-180 Regime PIT Rate |

| Uzbekistan-sourced Income | 12% | 12% |

| Foreign-sourced Income (Dividends, Rental, etc.) | 12% | 0% (Exempt) |

| Dividends from Local JSCs | Exempt (until 2028) | Exempt (until 2028) |

However, the non-refundable nature of the USD 50,000 fee makes preliminary tax modeling essential. For a high-net-worth individual with USD 1 million in annual foreign income, the fee is essentially a 5% "tax" for the first year, becoming more efficient in subsequent years as the status is valid for five years.

Residency by Investment and the Golden Visa Program

For individuals seeking more than just tax residency, Uzbekistan launched its first Residency by Investment (RBI) or "Golden Visa" program on June 1, 2025. This program provides a tiered pathway to residency and, eventually, naturalization based on the scale of capital commitment to the Uzbek economy.

Investment Pathways and Durations

The RBI program is structured to attract three types of capital: charitable donations, business expansion, and real estate development.

- Government Fund Donation: A one-time donation of USD 250,000 for the main applicant and USD 150,000 per family member grants an immediate 5-year residency permit. This is considered the fastest processing option for those who do not wish to manage local assets.

- Business Investment: Investing USD 250,000 into a local company secures a 3-year renewable residence permit. For larger industrial or production investments of USD 3 million, the government grants a 10-year renewable permit, reflecting a commitment to long-term industrialization.

- Real Estate Acquisition: Property purchase remains the most popular route for relocation, as it offers indefinite residency status. The required investment amount is tiered by geography to encourage regional development.

| Region | Minimum Investment (USD) | Residency Status |

| Tashkent (Capital City) | 300,000 | Indefinite/Permanent |

| Samarkand, Bukhara, Namangan | 200,000 | Indefinite/Permanent |

| Karakalpakstan & Other Regions | 100,000 | Indefinite/Permanent |

While foreigners can own buildings (residential and commercial), land ownership is restricted to Uzbek citizens and legal entities. Relocating investors must rely on long-term land leases, which are typically granted for up to 49 years.

Naturalization and Citizenship

Obtaining a residence permit through investment is a step toward citizenship, but Uzbekistan remains one of the few countries in the region that does not recognize dual nationality. Naturalization requires:

- Five consecutive years of legal residence.

- Proficiency in the Uzbek language.

- A lawful and stable source of income.

- Formal renunciation of other citizenships.

The IT Park Ecosystem: Relocation Incentives for Tech Firms

The "IT Park Uzbekistan" is the primary vehicle for the country’s digital transformation. By establishing a specialized legal and tax regime for information technology companies, the government has created one of the most attractive relocation destinations for tech firms in the CIS region.

The IT Visa: A Specialized Entry Portal

The IT Visa is a three-year multiple-entry visa designed for IT specialists, founders of IT companies, and investors. It removes several traditional hurdles, such as the requirement for a separate work permit.

| Category | Qualification Criteria | Benefits |

| IT Specialist | qualification in IT; USD 30,000+ income in last 12 months | No work permit needed; social rights equal to citizens |

| IT Founder | Must be a founder of a registered IT Park resident company | Multi-entry for 3 years; family eligibility |

| IT Investor | USD 10,000+ investment in a local IT company | Access to health and education services at local rates |

A critical detail for IT specialists is the verification of qualifications. The "Expert Council" of IT Park reviews applications within 20 working days. While a university diploma is standard, the regulation allows for "certificates or other documents" attesting to qualification, combined with a comprehensive resume. This flexibility acknowledges the non-traditional educational paths common in the software development industry.

Corporate Tax Holidays for IT Park Residents

For companies relocating their operations, IT Park membership provides a comprehensive exemption from major corporate taxes until 2028, with some benefits extended to 2040 for high-export firms.

- Corporate Income Tax (CIT): 0% (Standard 15%).

- Social Tax: 0% (Standard 12%).

- Personal Income Tax for Employees: 7.5% (Standard 12%).

- Dividends Tax: 5% for foreigners (Standard 10%).

- Customs Duties: Exemption for imported equipment for own use.

To maintain these benefits, companies must comply with the "List of Permitted Activities" and, for certain support programs, meet export thresholds. For example, the "Zero Risk" program provides free office space for 12 months and reimbursement of 15% of salaries for local employees, provided the company is export-oriented.

Employer of Record (EOR) vs. Entity Establishment

For many organizations, the strategic decision to relocate involves choosing between setting up a local subsidiary or using an Employer of Record (EOR). An EOR allows a company to hire local talent or relocate foreign specialists without establishing a permanent legal presence.

Comparative Analysis of Market Entry Models

| Feature | Local Entity Setup | Employer of Record (EOR) |

| Time-to-Market | 6–10 weeks | 2–5 days for local hires |

| Initial Cost | USD 2,000+ capital + legal fees | Service fee per employee |

| Administrative Burden | High (local accounting, audits, HR) | Low (managed by EOR) |

| Control | Total operational and legal control | Operational control; EOR handles legal |

| Compliance Risk | Borne by the company | Borne by the EOR |

| Best For | Long-term, large-scale presence | Testing markets, small teams, and remote work |

The "Employer of Record in Uzbekistan" model is particularly effective for navigating the recent 2025–2026 labor law changes. Uzbekistan’s Labor Code is complex and prohibits "at-will" employment; every termination requires a "just cause" and specific notice periods. An EOR mitigates these risks by issuing compliant contracts in both Uzbek and Russian, ensuring that all registrations in the Unified National Labor System (UNLS) are accurate.

The Legality of Outstaffing (Resolution 706)

Relocating firms must distinguish between standard EOR services and "outstaffing." In October 2024, Uzbekistan adopted Resolution No. 706, which formally legalized and regulated outstaffing. This regulation defines an outstaffer as a legal entity that transfers its in-house employees to a "receiving organization" under a specific agreement.

Key restrictions under Resolution 706 include:

- It is prohibited to outstaff employees to organizations abroad.

- Outstaffing is forbidden for "highly dangerous" facilities (e.g., explosive or radioactive materials).

- The outstaffer remains the party responsible for paying salaries and taxes, while the receiving organization must ensure workplace safety.

Labor Compliance and the UNLS Framework (2026)

The relocation of human capital to Uzbekistan requires adherence to the Unified National Labor System (UNLS), a digital ecosystem (my.mehnat) that has become the mandatory repository for all labor relations as of 2026.

Mandatory Digital Registration

Employers must now include granular details for every position in the UNLS, moving away from simple paper contracts. This includes:

- Qualification requirements and job duties.

- Specific working time regimes (5-day vs. 6-day weeks).

- Working conditions and guarantees for non-standard roles.

- Mandatory registration of all types of leave (vacation, maternity, sick).

The 2026 reforms also introduced "electronic administrative decisions." If the system detects a violation, such as a failure to register a contract or a violation of overtime limits, the authorities can issue fines automatically without a physical inspection of the employer's premises.

Working Hours and Overtime Limits

Standard working hours are set at 40 hours per week. In 2026, enforcement has sharpened regarding the compensation and duration of overtime.

| Metric | Regulation |

| Standard Week | 40 Hours |

| Max Daily (5-day) | 8 Hours |

| Overtime Rate | 1.5x (first 2 hrs), 2x (subsequent) |

| Max Overtime | 4 hrs over 2 days; 120 hrs per year |

| Night Work | Restricted and requires classification |

The shift towards 200% (2x) compensation for any work beyond standard hours or on public holidays is now a standard expectation in employment contracts.

Comprehensive Payroll and Taxation for 2026

Uzbekistan’s payroll taxes landscape is defined by the flat Personal Income Tax (PIT) and the Social Tax, both of which are withheld and remitted by the employer.

Tax Rates and Employer Contributions

For 2026, the baseline tax rates remain consistent with 2025, but the administrative thresholds have changed.

| Tax Type | Rate | Payer |

| Personal Income Tax (PIT) | 12% (Flat) | Employee (Withheld by Employer) |

| Social Tax (Standard) | 12% | Employer |

| Social Tax (Small Business) | 12% | Employer |

| Individual Pension Fund | 0.1% | Employer |

| Social Security (Mandatory) | 4.0% | Employee |

| Unemployment Insurance | 0.5% | Employee |

| Housing Loan Regime | 1.0% | Employee |

| Employee Training (INCES) | 0.5% | Employee |

Total employee contributions typically amount to 6% on top of the 12% PIT, while total employer costs add roughly 12.1% to the gross salary. It is important to note that for non-residents (those not under the UP-180 or IT Visa), the PIT rate for employment income from Uzbekistan sources remains 12% but applies only to local earnings.

Deadlines and Compliance Mechanisms

Employers must remit all PIT and social contributions to the State Tax Committee by the 15th of the month following the payroll cycle. In 2026, the "Unified Reporting System" (hisobot.gov.uz) allows business entities to submit 105 types of mandatory reports through a single portal, significantly reducing the bureaucracy of compliance for relocating firms.

Social Insurance Law (ZRU-1101) and Employee Benefits

The most significant change in the 2026 labor environment is the Law "On State Social Insurance," which transfers the payment of major benefits from the employer to the State Fund for Social Insurance.

Maternity and Childbirth Benefits

Effective January 1, 2026, maternity payments are no longer a direct liability of the employer. Instead, they are assigned automatically through the "Social Insurance" module based on "insurance experience".

- 10 to 24 months of experience: 75% of the average monthly salary.

- 25 to 60 months of experience: 85% of salary.

- 61+ months experience: 100% of salary.

The calculation considers the portion of the salary that does not exceed 10 times the minimum wage (approximately USD 1,000 as of 2026). This cap ensures the sustainability of the state fund while providing a baseline for all formal sector workers.

Sick Leave Pay (Transitioning July 1, 2026)

The responsibility for sick leave pay will be split between the employer and the state starting mid-2026.

- Employer Obligation: First 5 days of disability per calendar year.

- State Fund Obligation: From the 6th day until the end of the disability (up to 182 days).

The payout coefficients for sick leave have also been revised to favor long-term employees: 60% of salary for 6–96 months of experience and 80% for 97+ months. Previously, the rates were higher for shorter tenures (80% for 5 years), reflecting a policy shift toward rewarding labor force formalization and longevity.

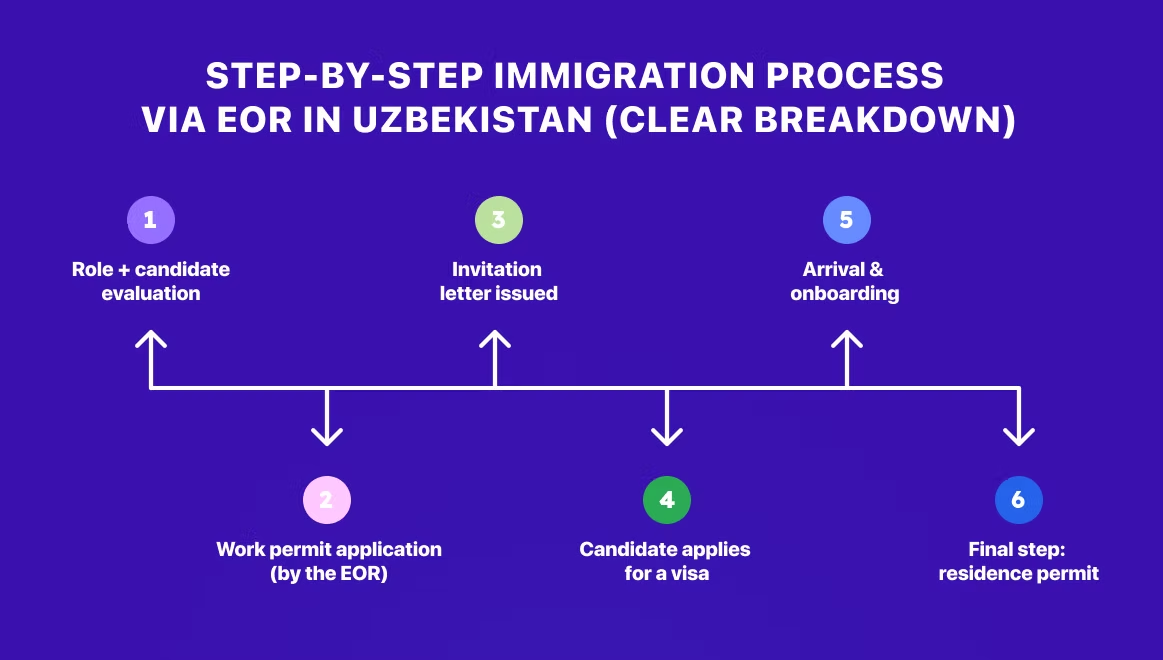

Practical Relocation Steps: Logistics and Integration

Beyond the legal frameworks of residency and taxation, relocating to Uzbekistan requires managing a series of practical, ground-level logistics. These range from digital identification to the "Rule of Three Days."

Mandatory Registration (Emehmon and PINI)

All foreigners staying in Uzbekistan must be registered at their place of stay within three working days. While hotels handle this automatically, individuals staying in private apartments or Airbnbs must ensure their hosts register them via the emehmon.uz portal.

Additionally, any foreigner engaging with the tax or banking system must obtain a Personal Identification Number of an Individual (PINI). This is a unique 14-digit number that serves as the primary identifier in the Unified National Labor System and for opening local bank accounts.

Financial and Technical Setup

- Authorized Banking: Under Decree UP-180, foreign residents must use "specially authorized" commercial banks. As of late 2025, the Central Bank is mandated to publish this list, which includes both state-capital banks (like NBU) and foreign-capital banks.

- SIM Card and UZIMEI: Relocating professionals have 30 days to register their mobile device's IMEI number with the UZIMEI system. Failure to do so results in the device being blocked from local networks. Registration requires a passport and a physical visit to a main post office or Uzimei center.

- Currency Controls: While foreign currency can be brought into the country (up to USD 6,400 without declaration), large-scale repatriation of profits is guaranteed by the 2019 Law on Investments, provided all tax obligations are met.

Housing and Property Ownership

Foreigners can purchase residential property, but the value of the property determines their residency rights. In Tashkent, the threshold is USD 300,000 for a permanent residence permit; however, those with an IT Visa can purchase property of any value and still receive residency benefits. This makes the IT Visa the most efficient path for middle-class tech professionals looking to relocate.

Comparison of Local EOR Providers for Relocating Companies

For companies choosing the EOR route, selecting a provider with "regional know-how" and automated compliance tracking is essential for the 2026 regulatory environment.

| Provider | Core Specialty | Key Advantage |

| ANCOR | Large-scale HR | Strong support for foreign worker registration and visas |

| Dataware | Remote Teams | Clear focus on IT and knowledge-based roles; guidance on tax residency |

| Smart Solutions | Audits & Payroll | Integrated accounting is useful for firms undergoing tax checks |

| Tax & Legal Uzbekistan | Compliance-First | Direct assistance with permits; legal and tax bundled together |

| Marillion | End-to-End HR | Practical help with ongoing compliance and statutory filings |

Providers like ANCOR and Smart Solutions are noted for their ability to handle the "complex paperwork" of foreign national registration, which is a frequent pain point for relocating firms.

Risk Mitigation: The "Gray Market" and Compliance Trends

A critical challenge for relocating firms is the prevalence of the "gray market"—unregistered labor or underreported salaries used to evade social taxes. In 2026, the Uzbek government has significantly increased the penalties for such practices through the "Interagency Hardware-Software Complex".

- Salary Transparency: The government is pushing for a minimum wage that constitutes at least 30% of GDP, necessitating real wage increases for formal sector employees.

- Trade Union Oversight: In organizations where a trade union is present, any termination of a contract must be agreed upon with the committee, adding a layer of social protection that foreign employers must navigate.

- AML/KYC Rigor: Authorized banks are now required to conduct deep AML/CFT compliance checks on the origin of funds for foreign residents. High-risk individuals may face denials of service if their source of wealth is not transparently documented.

Conclusion: Uzbekistan as a Regional Hub in 2026

The relocation to Uzbekistan in 2026 is no longer a venture into an administrative unknown but a structured move into an economy with clear, albeit sophisticated, legal requirements. The shift from the 183-day rule to the 30-day "Vital Interests" rule under Decree UP-180 provides unprecedented flexibility for global investors. Meanwhile, the IT Park ecosystem offers a fiscal sanctuary for digital exporters, provided they utilize formal employment structures like EOR or registered LLCs.

Success in relocation depends on three pillars: early digital registration in the UNLS and PINI systems, choosing the correct market entry vehicle (EOR vs. Entity), and maintaining proactive compliance with the new state social insurance fund. As Uzbekistan continues its march toward WTO accession and deeper global integration, the current window of aggressive tax incentives and residency reforms positions the Republic as the premier gateway to Central Asia.

Frequently Asked Questions

1. What is the difference between a "Corporate Work License" and "Individual Confirmation"?

To hire foreigners, a two-step approval is required. First, the Employer must obtain a "Permit" (Corporate Work License) to attract foreign labor. Second, each Employee must receive an "Individual Confirmation" (Work Permit). In 2026, the process is largely digitized through the my.mehnat.uz portal.

2. Are there exemptions for "Highly Qualified Specialists"?

Yes. If you hire a specialist with a university degree from a Top-1,000 international ranking and offer a salary of at least $60,000 USD/year, you do not need the Corporate Work License. The Individual Confirmation is issued for up to 3 years and can be extended indefinitely.

3. How does the "Local Labor Market Test" work?

For standard foreign hires, you must demonstrate that no local candidate was suitable. This involves posting the vacancy on the National Job Vacancy Database for at least 15 days. Only if no qualified local citizen is found can you proceed with the foreign hire application.

4. What are the mandatory social security changes as of January 1, 2026?

The new Law "On State Social Insurance" went into effect on Jan 1, 2026.

- State-Paid Benefits: Maternity and sick leave benefits are now progressively being moved to the State Fund for Social Insurance rather than being paid directly by the employer.

- Registration: All types of leave (sick, maternity, annual) must now be registered in the "Social Insurance" module of the Unified Social Protection Registry.

5. What are the 2026 tax rates for IT Park residents?

If your company is a resident of IT Park Uzbekistan, you benefit from the most competitive tax regime in the region:

- Corporate Income Tax: 0% (Exempt until 2028).

- Social Tax: 0% (Exempt).

- Personal Income Tax (PIT): Reduced to 7.5% for employees (compared to the national 12% flat rate).

6. Is there a minimum capital requirement for foreign-owned companies?

For a standard Limited Liability Company (LLC), there is no minimum charter capital requirement. However, for "Enterprises with Foreign Investment" (EFI), a minimum capital of roughly $33,000 USD (400 million UZS) is often required to unlock specific investor benefits and 3-year "INV" visas.

7. How strict are the "E-Contract" requirements?

As of 2026, all employment contracts must be registered in the Unified National Labour System (UNLS). The system now requires more granular data, including specific job duties, working conditions, and qualification requirements for each position. Failure to register within 5 days of hiring can lead to administrative fines.

8. What is the "Zero Risk Program" for new employers?

Launched by IT Park, this program allows export-oriented companies to minimize relocation costs. In 2026, it offers 12 months of free office space in the regions and reimbursement of up to $5,000 for personnel training and recruitment expenses.

9. Can I pay salaries in foreign currency (USD/EUR)?

Technically, no. All salaries must be paid in the national currency, Som (UZS). However, many employers index the salary to USD in the contract.

Practical Note: Salaries must be paid at least twice per month (an advance and a final payment) with a gap of no more than 16 days.

10. What are the 2026 penalties for illegal foreign employment?

Enforcement has tightened. Employing a foreigner without a valid "Confirmation" or working outside the approved location can result in fines up to 50 times the Base Calculation Value (BCV) for repeat violations, and the potential deportation of the employee.

.svg)