PEO vs Employer of Record (EOR) in Mexico: Which is right for your organization?

TL;DR

- PEO (Professional Employer Organization) and EOR (Employer of Record) are both HR outsourcing models — but they are not interchangeable, and the distinction matters enormously in Mexico's legal environment.

- A PEO operates as a co-employer: it shares employer liability with your company. You must already have a legal entity in Mexico for a PEO arrangement to function. If you do not have one, the PEO model cannot legally operate.

- An EOR is the sole legal employer. Your company has no Mexican entity. The EOR holds all employer obligations — LFT compliance, IMSS, INFONAVIT, SAT payroll, CFDI 4.0, and work permit sponsorship — on your behalf.

- The 2021 Mexican subcontracting reform (reforma de subcontratacion) fundamentally changed the PEO landscape in Mexico. Most traditional PEO structures are now legally non-compliant unless the provider holds active REPSE registration and operates within the narrow permitted scope of specialised services.

- For companies without a Mexico entity — which describes the majority of international companies entering the market — the EOR is not just the better option. It is the only legally viable one.

- For companies with an established Mexico subsidiary and 50+ employees, a PEO can provide meaningful HR administration support. But payroll compliance, IMSS management, and statutory benefit obligations remain the company's direct responsibility.

- Team Up operates exclusively as an EOR — not a PEO — because the EOR model is the structure that delivers genuine compliance transfer and full employer liability assumption in Mexico's post-reform regulatory environment.

The PEO vs EOR Mexico question comes up in almost every conversation about building a compliant workforce in Mexico without getting buried in operational complexity. Both models promise to simplify HR. Both involve outsourcing some portion of the employer function. And both are marketed with enough overlapping language that the distinction can seem academic — until you discover, usually at the worst possible moment, that the model you chose does not actually do what you needed it to do.

The distinction is not academic. In Mexico's post-2021 legal environment, the difference between a PEO and an EOR is the difference between having a legal employer on record and not having one. Between being compliant with the subcontracting reform and being jointly liable for every payroll obligation you thought you had outsourced. Between being able to sponsor a work permit for a foreign hire and not having the legal standing to do so.

This article draws the line clearly. It explains what each model does, where each one works in Mexico, what the 2021 reform changed, and how to decide which structure is right for your specific situation — based on where your organisation currently stands, not where you hope to be in two years.

Table of Contents

- TL;DR

- What Is a PEO and How Does It Work in Mexico?

- What Is an Employer of Record (EOR) and How Does It Work in Mexico?

- The Core Difference Between PEO and EOR in Mexico

- How Mexico's 2021 Subcontracting Reform Changed the PEO Model

- PEO in Mexico: When It Actually Makes Sense

- EOR in Mexico: When It Is the Right Structure

- Payroll Compliance: PEO vs EOR in Mexico's Three-System Architecture

- Liability, Risk, and What Happens When Things Go Wrong

- PEO vs EOR Mexico: Full Comparison Table

- The Decision Framework: How to Choose Between PEO and EOR in Mexico

- How Team Up Approaches This: EOR Only, and Why That Matters

- Final Thoughts

- Frequently Asked Questions

What Is a PEO and How Does It Work in Mexico?

A Professional Employer Organization (PEO) operates through a co-employment arrangement. In the classic PEO model, your company and the PEO become joint employers of the same workforce. Your company retains operational control: you direct the work, set the scope, define the compensation, and make the hiring and firing decisions. The PEO takes on the administrative employer functions: payroll processing, benefits administration, tax filings, and HR compliance support.

Understanding the co-employment model in Mexico

The word "co-employment" is the defining characteristic. Both entities share employer status. In practice, this means the PEO can only function if your company already has a legal employer presence in the relevant jurisdiction — a registered entity, a tax identification number, and the regulatory standing to enter into an employer relationship under local law. Without that foundation, there is no co-employment arrangement. There is just an outsourced HR services contract with a company that does not carry your employer liability.

Why PEO services require a Mexican legal entity

In the United States, PEOs are a well-established industry. The National Association of Professional Employer Organizations (NAPEO) estimates that more than 200,000 US small and mid-sized businesses use PEOs, covering approximately 4 million employees. The US model works because the PEO registers as a co-employer with the IRS and state tax authorities, allowing it to pool workers' compensation coverage, administer benefits at scale, and manage payroll taxes within a legally recognised co-employment structure.

Mexico is not the United States. The legal recognition that makes US PEOs functional does not map to Mexican labour law in the same way, and the 2021 subcontracting reform specifically addressed and constrained third-party employer arrangements in ways that have fundamentally altered what a PEO can and cannot legally do in Mexico.

What Is an Employer of Record (EOR) and How Does It Work in Mexico?

An Employer of Record is the sole legal employer. Not a co-employer. Not a shared employer. The EOR holds every employer obligation under Mexican law — the employment contract is between the EOR and the employee, the IMSS registration is under the EOR's employer number, the CFDI 4.0 payroll receipts are issued by the EOR as the paying employer, and the liability for LFT compliance, payroll tax remittance, and statutory benefit obligations sits entirely with the EOR.

How the EOR model works without a local entity

Your company — the client — directs the day-to-day work. You define the role, set the performance expectations, manage the working relationship, and decide when a hire is made or when an employment relationship ends. But you are not the employer of record. The legal employment relationship is between the EOR and the employee, and that distinction is what gives the EOR model its compliance integrity in Mexico.

Why EOR providers become the legal employer in Mexico

The EOR model does not require your company to have a Mexican legal entity. The EOR is already the entity. It holds REPSE registration under the 2021 subcontracting reform, IMSS employer registration for all employees it onboards, active RFC status with SAT, certified PAC integration for CFDI 4.0 payroll receipt generation, and INFONAVIT employer registration. All of this infrastructure is in place before your first Mexico hire.

This structure is why global companies use international employer of record services to enter new markets without the three-to-six-month entity formation timeline, the capital investment in local legal infrastructure, or the ongoing management overhead of maintaining a subsidiary in a jurisdiction where they may have five employees and uncertain long-term headcount projections.

| The employment contract in an EOR arrangement names the EOR as the employer. Some companies are uncomfortable with this at first — it feels like the employee does not truly work for them. In practice, the working relationship is entirely managed by the client. The EOR is the legal structure. The client is the operational reality. Mexican employees working through reputable EOR providers understand this model and it creates no ambiguity in their day-to-day experience. |

The Core Difference Between PEO and EOR in Mexico

What Co-Employment Actually Means for Liability

In a PEO arrangement, liability is shared. When a Mexican employee files a wrongful termination claim, the claim lands against both the client company and the PEO as co-employers. When IMSS audits the employment arrangement, both entities are in scope. When the STPS (Secretaria del Trabajo y Prevision Social) conducts a labour inspection, both employers are responsible for demonstrating compliance. The PEO provides HR and payroll administration. It does not absorb employer risk. Your company retains it.

This shared liability structure is workable when your company has deep familiarity with Mexican labour law, a local legal team that can respond to STPS inspections and IMSS audits, and the operational infrastructure to manage employment compliance jointly with the PEO. For most international companies entering Mexico, none of those conditions apply.

What Sole Employment Actually Means for Compliance

In an EOR arrangement, the EOR carries the employer liability. A wrongful termination claim is a claim against the EOR as the named employer. An IMSS audit targets the EOR's employer registration. An STPS inspection evaluates the EOR's compliance with LFT provisions. The client company is not in the liability chain for these events — it is the party directing the work of the employees, which is a distinct legal relationship from the employment relationship itself.

This clean liability separation is why EOR services have become the default international hiring vehicle for companies that want genuine compliance transfer — not just administrative outsourcing. The EOR is not acting as your payroll agent. It is the employer. That distinction is the entire point.

How Mexico's 2021 Subcontracting Reform Changed the PEO Model

The reforma de subcontratacion, which came into force on April 23, 2021, is the single most important regulatory event for understanding the PEO vs EOR question in Mexico. Before the reform, companies routinely outsourced their entire workforce to a third-party staffing company — an empresa de servicios de personal — which served as the formal employer while the client company directed all work. This model was used primarily to reduce PTU (profit-sharing) liability, lower IMSS contribution costs, and simplify internal HR administration.

What the REPSE reform changed for outsourcing providers

The reform prohibited it. Outright. Under the post-reform rules, the outsourcing of personnel is prohibited except in one narrow circumstance: specialised services (servicios especializados) provided by a company registered in the REPSE — the Registro de Prestadoras de Servicios Especializados u Obras Especializadas. And even then, the specialised services must be outside the client company's core corporate purpose. A technology company cannot use a REPSE-registered provider to outsource its software engineers, because software engineering is its core purpose.

Why have many traditional PEO structures become non-compliant

What does this mean for PEOs specifically? Traditional PEO arrangements — where the PEO is the formal employer but the client directs work that falls within the client's core business — are now prohibited under Mexican law unless the PEO holds REPSE registration and the services genuinely qualify as specialised. Most PEO arrangements do not meet that standard. Companies that maintained pre-reform PEO structures without updating them after April 2021 are currently operating outside the legal framework introduced by the reform, whether they know it or not.

The EOR model, by contrast, is not a subcontracting arrangement in the sense targeted by the reform. The EOR is the employer of record — the genuine legal employer, not a staffing intermediary. The client is the operational manager of the work. That structure, properly documented and supported by active REPSE registration for any specialised service components, is compliant with the post-reform framework.

| The joint liability provision introduced by the 2021 reform is the compliance risk that most companies underestimate. If your company uses a PEO or staffing provider that is not REPSE-registered, and that provider fails to meet its payroll tax or IMSS obligations, the Mexican government can pursue your company for the outstanding amounts under the joint liability (responsabilidad solidaria) provisions of the reform. The liability does not stay with the provider. It follows the work. |

PEO in Mexico: When It Actually Makes Sense

The Conditions That Make a PEO Viable

A PEO arrangement in Mexico works — and works well — under a specific set of conditions that are worth stating clearly, because the PEO model is not inherently wrong. It is wrong for the situations where it is most frequently proposed.

A PEO is a sensible choice in Mexico when your company already has an established legal entity (SA de CV or SRL) in Mexico with active RFC registration, IMSS employer status, and REPSE registration where applicable; when your headcount is large enough (typically 100+ employees) that the administrative burden of payroll processing, benefits administration, and HR compliance genuinely exceeds your internal team's capacity; and when the nature of the services the PEO provides qualifies as specialised under the post-reform framework, meaning they fall outside your core corporate purpose.

In practice, this describes a mature Mexico operation — not a market entry. Companies that have been operating in Mexico for several years, have a local HR function, and want to outsource the operational complexity of payroll and benefits administration to a specialist provider can benefit from the PEO model. The PEO brings scale efficiencies in benefits sourcing, workers' compensation pooling, and HR technology. The client retains the employer relationship and the compliance responsibility.

The Conditions That Make a PEO a Problem

A PEO is the wrong choice when your company does not have a Mexican legal entity and is using the PEO to avoid forming one — this is not legally possible under the co-employment model. It is the wrong choice when the PEO is not REPSE-registered, because the post-reform joint liability provision makes the client company responsible for the PEO's compliance failures. And it is the wrong choice when the company needs work permit sponsorship for foreign national hires, because the PEO's co-employment status does not give it the independent legal standing to serve as the sponsoring employer for INM work permit purposes without your entity's direct involvement.

EOR in Mexico: When It Is the Right Structure

Market Entry Without Entity Formation

The most common use case for EOR services in Mexico is market entry. A company has identified Mexico as a strategic hiring location — for nearshoring, for talent access, for client proximity — and needs to hire one to fifty employees without the three-to-six-month timeline and MXN 100,000 to 300,000 upfront cost of forming a local SA de CV. The EOR is the legal employer from day one. The first hire can be onboarded within three to five business days. IMSS registration is completed before the start date. The first payroll run is CFDI 4.0 compliant.

International Talent Relocation With Work Permit Sponsorship

Companies relocating experienced managers or technical specialists from other markets into Mexico-based roles need a registered legal employer to sponsor work permits through INM. The EOR is that employer. It holds REPSE registration, IMSS employer status, and the legal standing required for INM visa sponsorship. A company without a Mexico entity cannot sponsor work permits independently, and a PEO operating under co-employment cannot sponsor independently without the client entity's direct INM registration.

Compliance-First Operations in a High-Enforcement Environment

Mexico's STPS has increased inspection activity significantly since the 2021 reform. The political environment has been consistently pro-labour. The compliance baseline is not going down. For companies that need to be able to demonstrate clean employment records — no misclassified contractors, no unregistered subcontracting arrangements, no CFDI gaps — the EOR model provides documentation integrity that a PEO co-employment arrangement inherently cannot. The EOR is the employer of record. Every employee has a correctly structured LFT employment contract. Every payroll run has a valid CFDI. Every IMSS contribution is current.

Market Testing Before Permanent Commitment

Not every Mexico operation becomes permanent. Some companies are testing a customer service function, piloting a nearshore engineering team, or responding to a single client relationship with a defined timeline. Forming a legal entity for a one-to-two-year market test creates exit complexity that can cost six to twelve months and significant management attention to unwind. The EOR model provides a clean entry and a clean exit — with termination obligations managed compliantly within the contractual notice period.

Payroll Compliance: PEO vs EOR in Mexico's Three-System Architecture

The Three Systems and Who Is Responsible

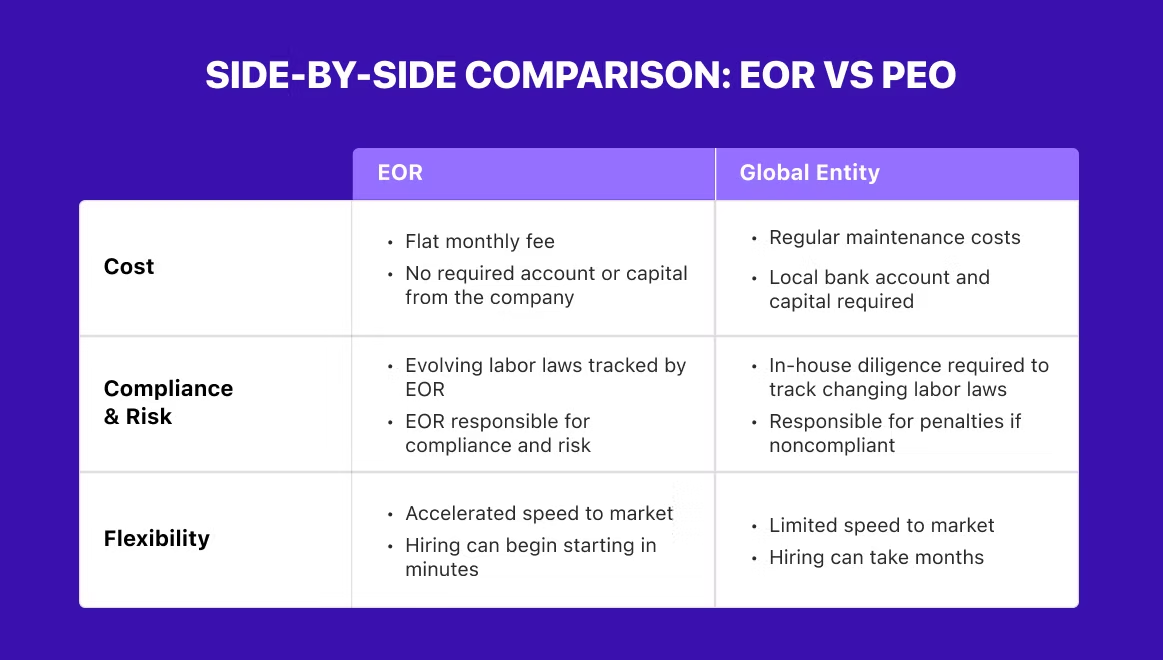

Mexican employer payroll compliance runs across SAT (federal income tax and CFDI), IMSS (social security contributions), and INFONAVIT (housing fund). Each system operates on a different filing cadence, uses a different platform, and applies penalties independently for late or incorrect filings. In a PEO co-employment arrangement, responsibility for these filings is shared, and shared responsibility in a complex regulatory environment is where errors accumulate. When both parties assume the other is managing a filing deadline, neither manages it.

In an EOR arrangement, the responsibility is unambiguous. The EOR is the employer of record. Every SAT CFDI, every IMSS bimonthly contribution, every INFONAVIT monthly filing is the EOR's operational responsibility. The client receives a consolidated payroll report. The compliance infrastructure runs entirely within the EOR's systems.

CFDI 4.0 and the Platform Question

CFDI 4.0 — the current mandatory version of Mexico's digital payroll receipt since January 2022 — requires certified PAC (Proveedor Autorizado de Certificacion) integration to generate and transmit digitally sealed XML documents to SAT within 72 hours of each payroll payment. A PEO may manage this on behalf of the client entity, but the CFDI is issued under the client entity's RFC. If the client entity's SAT registration has any irregularity — expired digital certificate, RFC under review, mismatched CURP data for an employee — the CFDI issuance fails, and the payroll payment has no valid tax documentation.

When the EOR issues the CFDI, it is issued under the EOR's RFC and digital certificate infrastructure — infrastructure that the EOR maintains as its core operational asset. The client company's SAT status is irrelevant to the CFDI issuance process. This is a meaningful operational resilience difference, particularly for companies entering Mexico for the first time, whose entity registrations may be newly established and subject to SAT verification delays.

Liability, Risk, and What Happens When Things Go Wrong

LFT Termination Liability

Mexico's Ley Federal del Trabajo is one of the most employee-protective frameworks in Latin America. Unjustified termination triggers a statutory severance package of three months' integrated daily salary plus 20 days per year of service — calculated on the full SDI, not the base salary, which is a distinction that materially affects the total. In a PEO arrangement, this liability is shared between the PEO and the client entity. The employee can bring a claim against either or both. The client entity is directly in the line of the claim.

In an EOR arrangement, the termination liability sits with the EOR as the named employer. The EOR manages the termination as a structured compliance event: assessing the cause against Article 47 of the LFT, calculating the correct integrated daily salary for severance purposes, producing the carta de finiquito, issuing the final CFDI, and completing the IMSS baja before the effective termination date. The client's exposure is limited to the contractual relationship with the EOR, not the direct LFT employment claim.

IMSS Audit Exposure

IMSS audits (revisiones de gabinete and visitas domiciliarias) can reach back five years. They examine SDI calculation accuracy, contribution timeliness, risk classification correctness, and the completeness of employee registration records. In a PEO arrangement, the client entity is an employer of record for IMSS purposes — the audit lands on your RFC. In an EOR arrangement, the audit lands on the EOR's employer registration. The EOR carries both the operational management of the employment records and the audit defence burden.

| If a PEO provider fails to remit IMSS contributions for your employees — whether through insolvency, operational failure, or deliberate avoidance — the 2021 reform's joint liability provision means IMSS can pursue your company for the outstanding contributions. This is not theoretical. It has happened to companies that assumed the PEO's financial obligations were the PEO's problem. With an EOR, you are a client contracting for services — not a co-employer carrying the underlying statutory obligation. |

PEO vs EOR Mexico: Full Comparison Table

The table below is structured for a decision-stage review — CFO, legal counsel, or HR leadership evaluating which model fits the specific situation. Every row maps to a real decision point, not a marketing claim.

| Decision Factor | PEO in Mexico | EOR in Mexico |

| Legal employer status | Co-employer (shared with client) | Sole employer of record |

| Requires client Mexico entity? | YES — entity required | NO — EOR is the entity |

| REPSE registration | Required — verify before engaging | EOR holds REPSE registration |

| 2021 reform compliance | Complex — most PEO models were affected | Compliant if EOR is REPSE-registered |

| IMSS employer registration | Client entity holds registration | EOR holds registration |

| CFDI 4.0 payroll receipts | Issued under client RFC | Issued under EOR RFC |

| LFT termination liability | Shared — client entity in claim line | Assumed by EOR as named employer |

| IMSS audit target | Client entity is audit target | EOR is audit target |

| Work permit (INM) sponsorship | Requires client entity INM registration | EOR sponsors independently |

| PTU (profit sharing) | Calculated on client company profits | Managed by EOR per fiscal results |

| Time to first hire | 3–6 months (entity formation first) | 3–5 business days |

| Suitable for companies without entity | NO | YES |

| Best suited headcount range | 100+ employees, permanent operations | 1–50 employees, any stage |

| Market exit flexibility | Tied to the entity dissolution timeline | Wind-down within notice period |

| Suitable for international talent relocation | Complicated — client entity involvement needed | Yes — EOR sponsors directly |

The Decision Framework: How to Choose Between PEO and EOR in Mexico

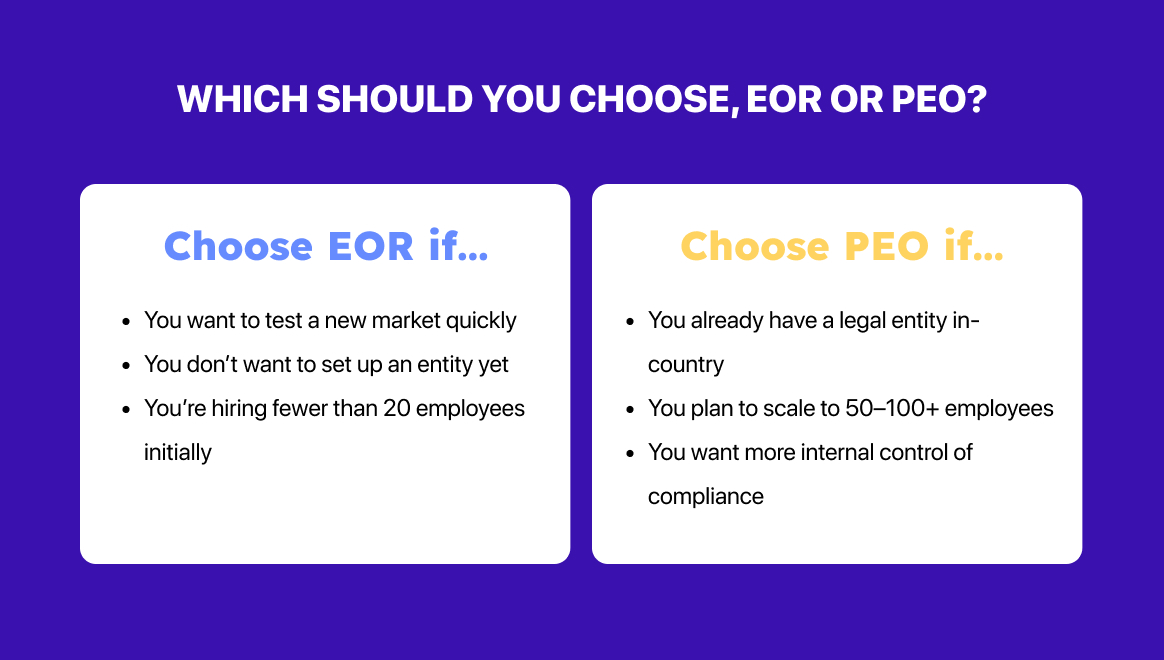

Start with the Entity Question

The first question is binary: Does your company have a registered legal entity in Mexico? If the answer is no, the PEO model is not available to you as a genuine co-employment arrangement. You are looking at an EOR, or at entity formation followed by a PEO engagement at some future point when headcount and permanence justify it. There is no grey area here. The co-employment model requires a co-employer on the client side. Without an entity, that co-employer does not exist.

Then, apply the Headcount and Timeline Test

If you have a Mexico entity, the next question is headcount size and operational maturity. Below 50 employees, the EOR almost always delivers better unit economics than maintaining a PEO relationship alongside a local entity: you are paying both entity maintenance costs and PEO fees. Above 100 employees with a permanent, established operation, the PEO can provide genuine administrative efficiency through benefits pooling, HR technology, and payroll processing scale. Between 50 and 100, the answer depends on the specific composition of your workforce, the complexity of your benefits structure, and whether you have internal HR capacity to manage the shared compliance obligations of a PEO co-employment arrangement.

Then Consider the Work Permit Need

If any of your Mexico hires require work permit sponsorship — foreign nationals relocating from other markets, intracompany transfers, or specialist hires requiring Temporary Resident Worker Visas — the EOR model provides cleaner sponsorship infrastructure. The EOR sponsors independently. The PEO requires your entity to be the primary INM-registered employer, which adds operational steps and timeline.

Finally, Assess Your Risk Tolerance

If your organisation needs to be able to demonstrate clean, unambiguous employer-of-record status in the event of an STPS inspection, an IMSS audit, or an employee labour claim — and most international companies operating in Mexico need exactly that — the EOR model provides documentation clarity that the co-employment structure cannot. Every employee has one employer of record. Every payroll run has one CFDI issuer. Every IMSS contribution sits under one employer RFC. The compliance record is clean and auditable.

How Team Up Approaches This: EOR Only, and Why That Matters

Team Up operates exclusively as an Employer of Record — not as a PEO, not as a staffing agency, not as a hybrid arrangement that shifts depending on the client's entity status. That choice is deliberate, and it reflects a view about what genuine compliance transfer actually requires in Mexico's post-2021 regulatory environment.

- Full employer liability assumption: Team Up is the employer of record on every employment contract. LFT obligations, IMSS contributions, INFONAVIT filings, CFDI 4.0 payroll receipts, PTU calculation and distribution — all of these sit with Team Up as the registered legal employer. The client does not carry them.

- REPSE registration: Team Up holds active REPSE registration, verifiable in the STPS public registry. This is the post-reform compliance requirement that distinguishes a legal employer arrangement from a prohibited subcontracting arrangement. No REPSE registration means no legal basis for third-party employment in Mexico.

- Work permit and visa sponsorship: Team Up can sponsor Temporary Resident Worker Visas and intracompany transfer visas for foreign nationals hired into Mexico roles — independently, without requiring the client to have a Mexico entity or INM employer registration.

- Multi-market coverage: Team Up's EOR infrastructure covers Mexico, Turkey, Georgia, Armenia, Azerbaijan, Kazakhstan, Uzbekistan, India, and MENA — using the same employer-of-record model, consistent reporting, and a single operational contact for clients hiring across multiple emerging markets.

- Transparent employer cost reporting: Every client receives a monthly report showing gross salary, IMSS contributions by branch, INFONAVIT obligation, statutory benefit accruals, ISR withholding, and the Team Up service fee as distinct auditable line items. No consolidated lump sums.

- Clean termination management: When employment ends, Team Up manages the full LFT termination process — severance calculation on the integrated daily salary, carta de finiquito, final CFDI, and IMSS baja — with documentation maintained for the five-year audit retention period.

Final Thoughts

The PEO vs EOR Mexico question has a clear answer for most international companies evaluating it seriously: if you do not have a Mexico entity, the EOR is not just the better model — it is the only model that is legally available to you. If you have an entity and 100-plus employees, a PEO can add genuine administrative value. For everything in between, the EOR delivers better compliance outcomes, cleaner liability transfer, and simpler operational management.

What the 2021 subcontracting reform made permanent is the requirement to be explicit about which entity is the legal employer. Shared employer arrangements without REPSE registration are now prohibited. Joint liability provisions mean that compliance failures by your employment service provider land on your company. The era of using a third-party HR provider as a compliance buffer without verifying its legal standing is over.

The EOR model — when operated by a REPSE-registered provider with genuine Mexico payroll infrastructure, active IMSS employer registration, and certified CFDI 4.0 capability — is the structure that delivers what most international companies actually need: legal employment from day one, transparent employer costs, compliant statutory benefit management, and the ability to scale or exit without carrying the infrastructure debt of a permanent entity.

Team Up is a REPSE-registered global employer of record operating across Mexico and key emerging markets in Eastern Europe, the Caucasus, Central Asia, and MENA. Contact the Team Up team to receive a clear employer cost breakdown for your Mexico headcount profile, a REPSE verification, and a concrete onboarding timeline for your first hire.

Frequently Asked Questions

Can a PEO legally operate in Mexico after the 2021 subcontracting reform?

Yes, but only in a narrow set of circumstances. A PEO can operate in Mexico post-reform if it holds active REPSE registration and the services it provides qualify as specialised — meaning they fall outside the client company's core corporate purpose. Most traditional PEO arrangements, where the PEO employs workers who perform the client's primary business functions, do not meet this standard. Companies that maintained pre-reform PEO structures without updating their compliance framework after April 2021 may be operating outside the legal requirements introduced by the reform.

Is it possible to use both a PEO and an EOR simultaneously in Mexico?

In theory, yes — a company could use an EOR for employees hired without a local entity and transition to a PEO arrangement for the same or different employees once a local entity is established. In practice, this is rarely the right structure because it creates two different employment frameworks within the same Mexico operation, which complicates HR administration, benefits standardisation, and STPS compliance documentation. Most companies that start with an EOR and build toward a permanent Mexico presence either transition entirely to a local entity with internal HR, or continue with the EOR model through their Mexico growth phase.

Does using an EOR in Mexico affect how employees experience their employment?

Employees hired through an EOR in Mexico have exactly the same LFT rights as employees of any other registered Mexican employer. Their employment contract names the EOR as the employer — which is legally required to be accurate — but their working relationship is entirely with the client company. Their IMSS coverage is active from day one. Their INFONAVIT contributions accumulate normally. Their Aguinaldo, prima vacacional, and PTU are calculated and paid on the same schedule as any other Mexico employer. Transparency about the EOR structure is both ethically correct and legally required under REPSE obligations.

What happens to the EOR model if my company later forms a Mexico entity?

The transition from EOR to local entity is a structured process involving employee transfer through novation agreements, IMSS employer registration transfer (baja patronal for the EOR, alta patronal for the new entity), CFDI continuity management during the transition period, and employment contract restating. A qualified EOR coordinates this transition as part of its client service. Seniority accruals continue without interruption, and statutory benefit obligations do not reset. Most companies initiate this transition when their Mexico headcount reaches 30 to 50 employees and the permanence of the operation is confirmed.

How does the PEO vs EOR choice affect PTU (profit-sharing) obligations in Mexico?

PTU is calculated on the company's taxable pre-tax profit declared to SAT. In a PEO arrangement, the client company is the employer for PTU purposes — the 10% distribution obligation is calculated against the client's Mexico entity fiscal results. In an EOR arrangement, the EOR manages the PTU distribution event, but the calculation is still tied to the client company's operational results as disclosed to the EOR. Neither model eliminates the PTU obligation — it is an LFT mandate that applies to any company with employees in Mexico. What the EOR does is manage the calculation, the two-pool distribution, the individual cap under the 2021 reform, and the ISR treatment of each payment.

If I use an EOR in Mexico, who is responsible if a payroll tax filing is late?

The EOR is responsible. As the employer of record, the EOR holds the obligations for ISR withholding remittances to SAT, IMSS bimonthly contributions, and INFONAVIT monthly filings. Late filing penalties accrue against the EOR's RFC and IMSS employer registration. The client company is not directly liable to the government for these filings — that liability sits with the EOR as the registered employer. This is a core distinction between the EOR and PEO models: in a PEO arrangement, late filings that occur under the client entity's RFC create direct liability for the client company.

Does the EOR or the PEO model work better for remote employees in different Mexican states?

The EOR model handles multi-state hiring more efficiently for companies without a Mexico entity. Each Mexican state imposes its own ISN (Impuesto sobre Nominas) payroll tax, ranging from approximately 1% to 4% of gross payroll. An EOR with established Mexico infrastructure manages ISN obligations across all 31 states and Mexico City from a single payroll system — no multi-state entity registrations required on the client side. A PEO operating under co-employment requires the client entity to maintain separate state-level compliance relationships. For distributed nearshoring teams spanning Monterrey, Guadalajara, and Mexico City, the EOR provides simpler, more consistent compliance management.

.svg)