Employee Benefits, Insurance & Workspace: What EORs Provide in Canada

Employer of record arrangements let foreign companies hire Canadian talent without a local entity. But the decision to use one hinges on practical questions about what you actually get. What benefits reach your employees? Who handles provincial healthcare gaps? What happens when your remote hire in Vancouver needs a workspace?

A London fintech company recently hired four customer success managers across Ontario and British Columbia through an EOR. Within 12 days, all four had signed compliant employment contracts, enrolled in group health coverage, and received home-office stipends. The company avoided a six-month incorporation process entirely.

Canada's employment landscape splits across 13 provincial and territorial jurisdictions. Each sets its own vacation minimums, statutory holiday calendars, and employment standards. Quebec adds an entirely separate pension and parental insurance system. For a foreign employer with no Canadian legal presence, managing this patchwork alone takes either a local entity or an EOR that absorbs the complexity on your behalf.

What Is an Employer of Record?

Employer of Record Definition and Legal Role

An employer of record is the legal entity that employs workers on behalf of another company. The EOR appears on payroll records, tax filings, and government remittances. It bears the legal obligations of an employer under Canadian law.

The client company directs the employee's daily work. It sets projects, manages performance, and controls deliverables. The EOR handles the employment relationship from a compliance standpoint. It remits payroll taxes and statutory deductions to the Canada Revenue Agency.

This split matters legally. The CRA treats the EOR as the employer for tax purposes. That means CPP contributions, Employment Insurance premiums, and income tax withholdings flow through the EOR's payroll account. The client company's name does not appear on the T4 slip.

How an EOR Differs from a PEO in Canada

A professional employer organization operates under a co-employment model. Both the PEO and the client share employer responsibilities. The client must already have a Canadian legal entity for the PEO arrangement to work.

An EOR eliminates that requirement. The foreign company needs no Canadian incorporation, no CRA business number, no provincial registration. The EOR is the sole legal employer. This is the structural difference that drives most foreign companies toward the EOR model when entering Canada for the first time.

Why Foreign Companies Use EORs to Enter Canada

Setting up a Canadian subsidiary takes months. You need federal or provincial incorporation, a CRA business number, provincial employer health tax registrations, and workers' compensation board accounts. A US SaaS company with three planned hires in Toronto would spend more on legal and accounting setup fees than on six months of EOR service.

EOR arrangements compress that timeline to days. The employee starts under a compliant contract while the client retains full operational control. For companies testing the Canadian market before committing to a permanent entity, the EOR model in Canada removes the upfront capital and administrative burden entirely.

What EOR Services Include in Canada

Payroll Administration and CRA Remittance

The EOR runs payroll on the schedule the client chooses. It calculates gross-to-net pay, applies federal and provincial tax rates, and deducts Canada Pension Plan contributions and Employment Insurance premiums. Every pay cycle, the EOR remits these amounts to the CRA under its own payroll account.

Provincial employer health taxes add another layer. Ontario, British Columbia, Manitoba, and Newfoundland each impose employer-side health levies with different thresholds. The EOR tracks which provinces apply, calculates the correct amounts, and files accordingly.

Year-end obligations fall on the EOR as well. It issues T4 slips to employees and files T4 summaries with the CRA. For employees in Quebec, the EOR also files Relevé 1 slips with Revenu Québec. A Dublin-based gaming studio that hired seven developers across three provinces through an EOR reported zero payroll filing errors in its first full tax year.

Employment Contracts and Provincial Compliance

Canadian employment law is not uniform. Each province sets its own employment standards. Minimum notice periods, overtime thresholds, and statutory holiday entitlements differ between Ontario and Alberta, between British Columbia and Quebec.

The EOR drafts employment contracts that comply with the employee's home province. It builds in the correct probationary period language, termination provisions, and overtime rules. When legislation changes mid-contract, the EOR updates terms to stay current.

Onboarding, Offboarding, and Record of Employment Issuance

Onboarding through an EOR typically completes in 5 to 10 business days. The EOR collects tax forms, banking details, and benefit enrollment preferences. It registers the employee with the relevant provincial workers' compensation board.

When employment ends or earnings are interrupted, the EOR issues a Record of Employment (ROE). The ROE is an official document that Service Canada requires for Employment Insurance claims. The EOR bears the legal obligation to issue it accurately and on time.

| Service Component | What the EOR Handles |

|---|---|

| Payroll processing | Gross-to-net calculation, tax withholding, direct deposit |

| CRA remittance | CPP, EI, and income tax filings under EOR's account |

| Provincial health tax | Employer health levies in applicable provinces |

| Employment contracts | Province-specific terms, probation, termination clauses |

| Onboarding | Tax form collection, benefit enrollment, WCB registration |

| ROE issuance | Official Record of Employment upon earnings interruption |

| Year-end filing | T4/T4A slips, Relevé 1 (Quebec), T4 summaries |

Employee Benefits Provided by EORs in Canada

| Benefit Category | Statutory (Mandatory) | Supplemental (EOR-Provided) |

|---|---|---|

| Pension | CPP contributions (QPP in Quebec) | Group RRSP matching programs |

| Employment protection | EI premiums | Top-up policies for parental leave |

| Vacation | Provincial minimum entitlements | Additional paid days above statutory floor |

| Health coverage | Provincial public healthcare | Extended health, dental, vision plans |

| Parental leave | Federal/provincial job protection | QPIP premiums in Quebec; salary top-ups |

| Disability | Workers' compensation (workplace) | Short-term and long-term disability insurance |

Mandatory Statutory Benefits: CPP, EI, and Vacation Entitlements

Every EOR operating in Canada must remit Canada Pension Plan (CPP) contributions for both employer and employee shares. CPP is mandatory across all provinces except Quebec. The contribution rate is set annually by the federal government and applies to earnings within a defined band.

Employment Insurance (EI) premiums are the second statutory pillar. Both employer and employee contribute, with the employer paying a higher share. The EOR deducts the employee portion from each paycheck and remits both shares to the CRA.

Vacation entitlements form the third mandatory layer. Every province sets a minimum. Most provinces mandate at least two weeks of paid vacation after one year of service. Several provinces increase the minimum after five or more years of employment. The EOR tracks tenure and adjusts entitlements accordingly.

Quebec-Specific Obligations: QPP and QPIP

Quebec operates outside the CPP system entirely. Employees working in Quebec contribute to the Quebec Pension Plan (QPP) instead. The QPP mirrors CPP's structure but uses its own contribution rates and ceiling, both set by Revenu Québec.

Quebec also mandates the Quebec Parental Insurance Plan (QPIP). QPIP provides parental, maternity, paternity, and adoption benefits. Both employer and employee pay premiums. No other province has an equivalent mandatory program at this scale. An EOR hiring in Quebec must register separately with Revenu Québec and remit QPP and QPIP premiums through a distinct filing process.

A Copenhagen e-commerce company hired two product managers in Montreal through an EOR. The EOR handled the Revenu Québec registration, Relevé 1 issuance, and QPP/QPIP remittance. The client's finance team never touched a provincial tax form.

Supplemental Benefits: Extended Health, Dental, and Vision

Canada's provincial healthcare systems cover physician visits and hospital care. They do not cover prescription drugs, dental care, vision care, or paramedical services like physiotherapy. This gap is where supplemental employer benefits become critical for talent attraction.

EORs in Canada typically offer group plans that bundle extended health, dental, and vision coverage. These plans cover prescription medications, dental cleanings and major dental work, eye exams, and corrective lenses. Some EORs include paramedical coverage for massage therapy, chiropractic care, and mental health counseling.

How EORs Structure Competitive Benefits Packages

The Canadian talent market expects supplemental health coverage as a baseline. A software engineer in Toronto evaluating two offers will compare dental and vision plans alongside salary. EORs understand this dynamic.

Most EORs offer tiered benefit structures. A basic tier covers core extended health and dental. A premium tier adds life insurance, accidental death coverage, and higher paramedical limits. Some EORs allow the client to customize the tier per employee or per role level, giving the client flexibility without administrative overhead.

Health Insurance and Workspace Provisions

Provincial Healthcare vs. Employer-Provided Private Health Plans

Every Canadian province and territory runs its own public health insurance plan. These plans cover medically necessary physician services and hospital stays. They do not cover most prescription drugs outside hospital settings. They do not cover dental, vision, or mental health counseling.

New employees moving between provinces face a waiting period before provincial coverage activates. Ontario and British Columbia impose a three-month wait. During this gap, the employee has no public coverage. A strong EOR bridges this window with interim private health insurance from day one.

Extended Health Benefits EORs Commonly Provide

The extended health plans that EORs arrange typically cover four categories. Prescription drugs represent the largest cost component. Dental coverage ranges from preventive cleanings to major restorative work. Vision coverage includes annual eye exams and a fixed allowance for corrective lenses. Paramedical benefits cover practitioners like physiotherapists, psychologists, and registered massage therapists.

A Chicago-based digital agency hired a UX researcher in Calgary through an EOR. The employee's group plan included $2,000 in annual paramedical coverage and full prescription drug coverage with a modest copay. The agency reported that the benefit package helped them compete against a local Canadian company offering a similar salary.

Workspace Solutions for Remote and Hybrid Canadian Employees

Most EOR-hired employees in Canada work remotely. The EOR cannot mandate where the employee works, but it can provide workspace support that shapes the experience. Two models dominate.

Home-office stipends cover the cost of setting up a productive workspace. Common items include ergonomic chairs, external monitors, and high-speed internet subsidies. EORs typically administer these as a one-time onboarding allowance or an annual recurring stipend.

Coworking space allowances give employees access to shared offices. The EOR either reimburses monthly coworking memberships or partners with coworking networks to offer direct access. For employees in cities like Toronto, Vancouver, or Montreal, this solves the isolation problem that remote workers frequently cite.

A Berlin data analytics firm hired five analysts across Canada through an EOR. Each received a home-office setup allowance during onboarding and a monthly coworking budget. The firm credited the workspace provisions with reducing early attrition compared to previous hires who received no such support.

How to Evaluate and Select an EOR for Canadian Benefits

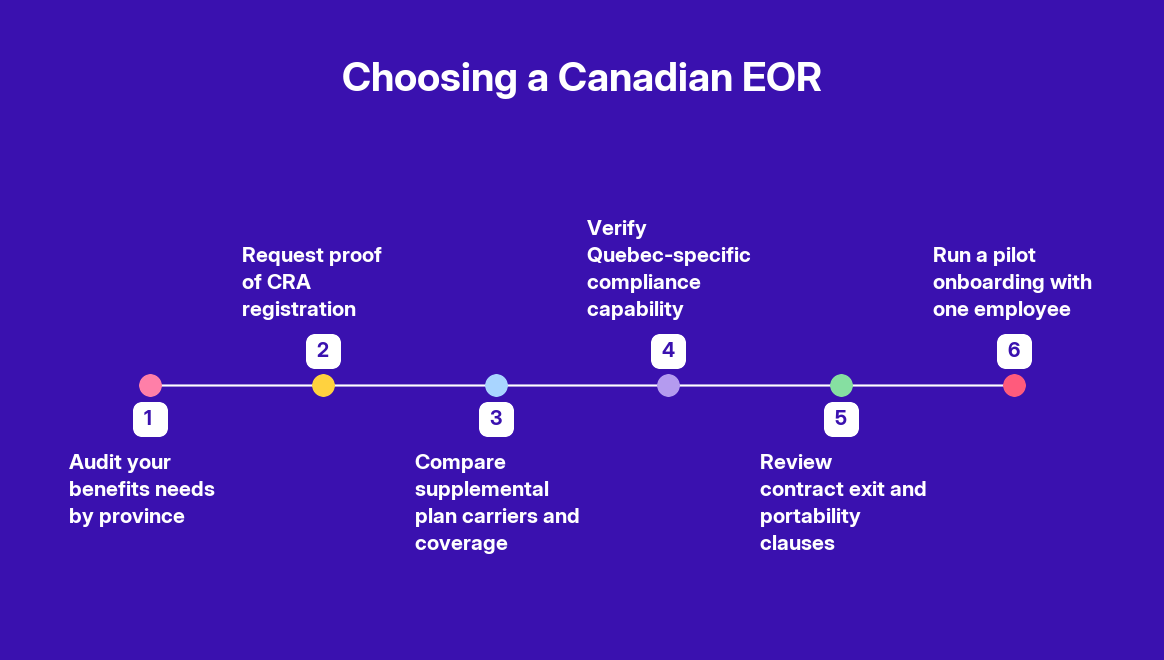

Start with a province-level audit of your workforce. An employee in Ontario has different statutory holiday entitlements than one in British Columbia. An employee in Quebec requires enrollment in the QPP rather than CPP. Your EOR must demonstrate the operational capacity to handle these distinctions without manual prompting from your team.

Request proof that the EOR holds active CRA payroll accounts. Ask for the Business Number under which your employees will be registered. A legitimate employer of record files remittances under its own BN, not yours. That separation is the structural reason you can hire in Canada without a local entity.

Scrutinize the supplemental benefits package. Ask which insurer underwrites the group plan. Ask whether dental, vision, and paramedical coverage come from one carrier or multiple. A Copenhagen fintech evaluating EORs for its first three Canadian hires rejected one provider whose extended health plan excluded mental health practitioners. The firm chose a second EOR whose plan included psychology and physiotherapy coverage. That decision reduced benefits-related complaints to zero in the first year.

Check the exit clause. If you later incorporate a Canadian entity, you need a clean transition path. The EOR should outline how it transfers employee records, outstanding benefit claims, and accrued vacation balances. Ask whether employees keep their group benefits during a transition period or face a coverage gap.

Run a pilot. Onboard one employee before committing to a larger team. Track the payroll cycle, benefits enrollment timeline, and first CRA remittance. A successful pilot takes five to ten business days and reveals operational quality faster than any sales presentation.

EOR-Provided Benefits vs. Direct-Entity Benefits in Canada

Choosing between an EOR and your own Canadian entity shapes the benefits experience for every employee. The operational differences go beyond cost. They affect compliance speed, plan flexibility, and your exposure to CRA audits.

| Factor | EOR-Provided Benefits | Direct Entity Benefits |

|---|---|---|

| Setup timeline | 5-10 business days | 3-9 months for incorporation and registration |

| CRA registration | EOR holds the BN and files remittances | You register directly with CRA |

| Group plan enrollment | Employees join the EOR's existing plan | You negotiate and bind a new group plan |

| Quebec compliance | EOR manages QPP and QPIP enrollment | You register separately with Revenu Québec |

| Plan customization | Limited to EOR's carrier options | Full control over plan design and carrier |

| Exit complexity | Transition clause governs portability | No transition needed; you own the plan |

| Administrative burden | EOR handles ROEs, T4s, remittances | Your HR or payroll team owns every filing |

A direct entity gives you full control over plan design. You can choose your insurer, set contribution splits, and add perks like fertility coverage or executive health assessments. That control comes with a cost. You need a Canadian payroll team or an outsourced payroll provider, a benefits broker, and ongoing compliance monitoring.

An EOR compresses the administrative surface. A New York e-commerce brand with four customer support agents in Toronto used an EOR to avoid hiring a Canadian HR manager. The EOR's group plan covered extended health, dental, and an Employee Assistance Program. Eighteen months in, the company had scaled to eleven agents without adding any Canadian back-office headcount.

The trade-off is customization. EOR group plans serve multiple client companies under one policy. You cannot easily carve out a bespoke fertility benefit or a premium executive tier for one client's employees. If deep plan customization matters, a direct entity or a PEO arrangement offers more latitude.

For companies hiring fewer than fifteen employees in Canada, the EOR model typically delivers faster compliance and lower fixed costs. Above that threshold, the economics of a direct entity begin to improve. The break-even point depends on your industry, the provinces you operate in, and how much plan customization your talent strategy demands.

FAQs

What happens to an employee's benefits if the EOR vendor shuts down or exits the Canadian market?

Your employment contract typically includes a continuity clause requiring the EOR to provide 30 to 90 days notice before market exit. During that window, you must either transition employees to a new EOR or incorporate your own entity. The critical risk is timing. If the EOR ceases operations before filing outstanding CRA remittances or issuing Records of Employment, that liability can fall to you as the de facto employer. Unpaid CPP and EI contributions accrue interest and penalties under CRA rules. Review your contract's exit provisions before signing.

Can an EOR provide benefits to a Canadian contractor who is later reclassified as an employee?

An EOR can enroll the reclassified worker in its benefits plan going forward. The deeper problem is retrospective. Reclassification triggers back-payment obligations for CPP and EI contributions, potentially spanning the entire contractor engagement period. CRA applies penalties and interest on those unpaid amounts. The EOR arrangement does not shield you from reclassification exposure if the original working relationship was misstructured. CRA examines the substance of the arrangement, not which entity holds the contract. Fix the classification before it becomes a liability.

Does an EOR need to provide separate benefit plans for Quebec employees versus employees in other provinces?

Yes, Quebec requires distinct treatment on multiple levels. Employees in Quebec enroll in the Quebec Pension Plan (QPP) instead of CPP. They also contribute to the Quebec Parental Insurance Plan (QPIP) instead of relying solely on federal EI for parental benefits. Group insurance plans may need Quebec-specific riders or separate insurer agreements to comply with provincial insurance regulations. A competent EOR manages these enrollments automatically. Ask your EOR whether its group plan carrier is licensed in Quebec and whether the plan meets Régie des rentes and QPIP requirements.

How does an EOR handle a Canadian employee who moves from one province to another mid-employment?

The EOR must update the employee's jurisdiction of work. This triggers several changes at once. Employment standards shift to the new province, affecting vacation entitlements, statutory holidays, and termination notice periods. Payroll tax remittance rules update because provincial tax rates differ. If the employee moves to or from Quebec, the pension and parental insurance programs change entirely. The EOR bears the compliance burden of making this transition without gaps. Ask your EOR how quickly it processes inter-provincial moves and whether it adjusts benefits enrollment automatically or requires manual notification.

Are EOR-provided workspace stipends or coworking allowances taxable as employment benefits in Canada?

CRA treats workspace allowances differently depending on their structure. A flat monthly stipend paid regardless of actual expenses is generally a taxable benefit. The EOR must include it on the employee's T4 slip. Reimbursements for specific home-office expenses, supported by receipts, may qualify as non-taxable under CRA's home-office expense guidelines. The distinction depends on whether the employer requires the employee to work from home and whether the reimbursement reflects actual costs. The EOR, as legal employer, makes this determination and bears the filing responsibility.

Can an EOR offer different benefit tiers to different employees within the same client company?

Most EOR group plans apply uniform coverage across all employees enrolled under one client agreement. Creating separate tiers, such as executive health assessments for senior hires or enhanced dental for a specific role, requires the EOR's insurer to support sub-group classifications. Not all carriers permit this. If tiered benefits matter to your retention strategy, confirm during the evaluation phase whether the EOR's plan structure supports sub-groups. Some EORs offer supplemental benefits riders that layer on top of the base plan, giving partial flexibility without requiring a custom group policy.

What is the EOR's liability if it fails to remit CPP or EI contributions on time?

The EOR, as the legal employer, bears direct liability for late or missed remittances to CRA. Penalties start at 3% for amounts one to three days late and escalate to 10% for amounts more than seven days overdue. CRA also charges compound daily interest on the outstanding balance. If the EOR fails to remit, CRA does not pursue your company directly, as long as the EOR relationship is properly structured. Your risk surfaces if the EOR becomes insolvent or if CRA determines the EOR arrangement lacks substance. Review the EOR's remittance history and financial stability before signing.

What to Watch Next

Several Canadian provinces are reviewing employment standards legislation. British Columbia and Ontario have both signaled potential updates to gig worker classification rules. Those changes could affect how EORs structure contractor arrangements in those provinces.

Federal discussions around portable benefits continue. A portable benefits framework would let workers carry coverage between employers and platforms. If adopted, it would reshape how EORs design supplemental plans.

Monitor CRA's evolving guidance on remote work deductions and employer-paid home-office allowances. The rules tightened after pandemic-era flexibility. Your EOR should track these updates and adjust T4 reporting accordingly.

Your concrete next step: request a benefits audit from your current or prospective employer of record in Canada. Ask for a province-by-province breakdown of statutory obligations, supplemental plan details, and the exact CRA filing cadence for your team size.

.svg)