Local vs Global Employer of Record (EOR) in Turkey: A Comprehensive Guide

Tl;DR

The strategic landscape of global expansion has undergone a fundamental transformation, shifting from a model of rigid corporate localization to one of agile, talent-centric deployment. For organizations targeting the Turkish market, this shift is mediated by the legal and operational framework of the Employer of Record (EOR).

Turkey presents a unique paradox: it offers a highly skilled, cost-competitive workforce at a geographical crossroads between Europe, the Middle East, and Central Asia, yet it possesses one of the most complex and litigious labor environments in the world.

Navigating this environment requires a nuanced understanding of the Turkish Labor Law No. 4857, the Social Security and General Health Insurance Law No. 5510, and the evolving administrative practices of the Social Security Institution (SGK) and the Turkish Revenue Administration (GIB).

Quick navigation

- Tl;DR

- The Strategic Role of the EOR in the Turkish Market

- Legal Foundations: Turkish Labor Law No. 4857

- Comparative Analysis: Global vs. Local EOR Models

- Financial Compliance: Payroll, Taxation, and Social Security

- The 2026 Social Security Reforms (Omnibus Law No. 7566)

- Statutory Benefits and Local Market "Perks"

- Termination, Severance, and Notice Periods

- Temporary Employment and the "Article 7" Risk

- Risks of Misclassification and Permanent Establishment

- Licensing and Private Employment Agencies (İŞKUR)

- Navigating the Work Permit Landscape

- Strategic Considerations for Provider Selection

- Conclusion: Synthesis and Future Outlook

- Frequently asked questions

The Strategic Role of the EOR in the Turkish Market

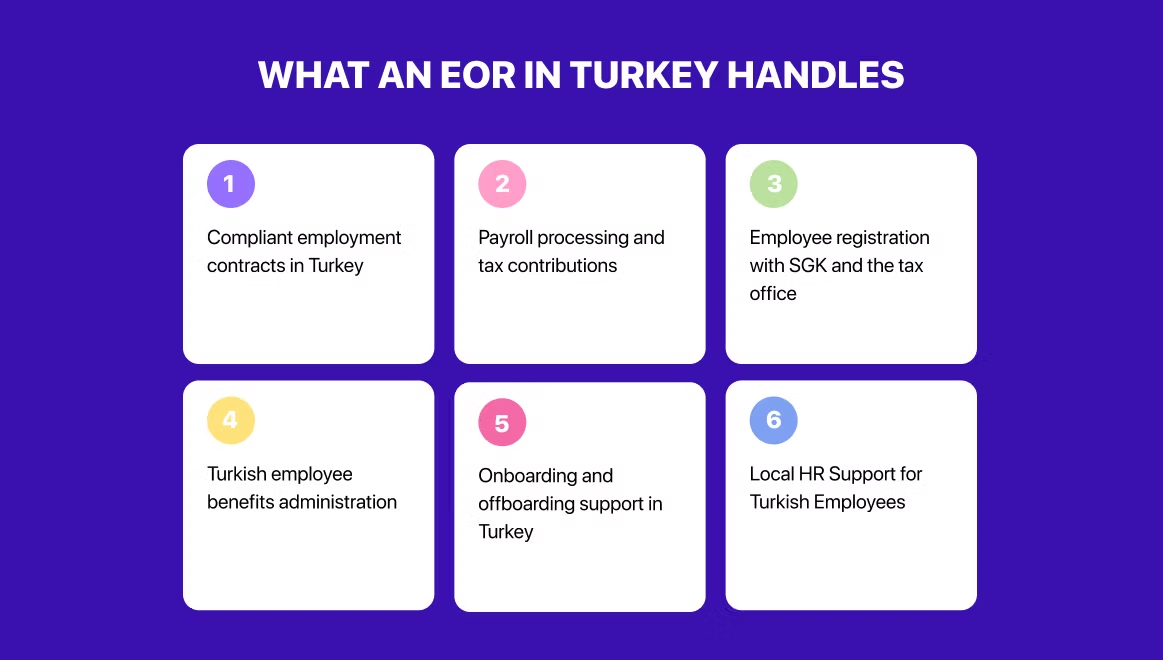

An Employer of Record in Turkey serves as a bridge for foreign enterprises that lack a local legal presence but wish to engage talent directly within the national territory. Under this arrangement, the EOR becomes the official employer on paper for all legal, tax, and compliance purposes, while the client company maintains full operational control over the employee's day-to-day responsibilities and work product. This mechanism is particularly valuable for businesses testing the Turkish market, those needing to hire specific skill sets urgently, or organizations wishing to avoid the "Permanent Establishment" (PE) risks that trigger corporate tax obligations.

The alternative to an EOR, establishing a local subsidiary, branch, or representative office, is a significant commitment. Setting up a Turkish entity can take months and involves substantial upfront costs, legal fees, notary requirements, and minimum capital injections. For example, establishing a joint-stock company requires a minimum capital of 50,000 TRY, while a limited liability company requires 10,000 TRY, alongside complex registration with the Central Registry System (MERSIS). By contrast, an EOR allows for onboarding in as little as three to five days.

| Criteria | Direct Employer (Local Entity) | Employer of Record (EOR) |

| Entity Setup | Required (Subsidiary/Branch) | Not required |

| Time to Hire | 3–12 months | 2–5 business days |

| Regulatory Liability | Full and direct liability | Shared/EOR holds primary legal liability |

| Capital Investment | High (Notary, legal, capital) | Low (Monthly service fees) |

| HR/Payroll Management | Internal team required | Outsourced to EOR |

| IP Protection | Direct contractual chain | Managed through the EOR framework |

Legal Foundations: Turkish Labor Law No. 4857

The primary statute governing employment relationships in Turkey is the Labor Law No. 4857, adopted in 2003 to align with European Union labor standards. Article 1 explicitly states that the Act's purpose is to regulate the working conditions and work-related rights of employers and employees working under an employment contract. The law applies to almost all establishments and employees within the national territory, with specific exceptions detailed in Article 4, such as maritime and air transport, family businesses, and agricultural enterprises with fewer than 50 workers.

The law defines an "employee" as a real person working under an employment contract and the "employer" as a real or corporate person or non-corporate institution employing such persons. A critical concept for foreign firms is the "employer's representative," who acts on behalf of the employer and is charged with the direction of the work and the establishment. Crucially, the employer is directly liable for the conduct and responsibilities of their representative.

Non-Discrimination and Equal Treatment

Article 5 of the Labor Law enshrines the principle of non-discrimination, prohibiting employers from discriminating based on language, race, color, gender, disability, political opinion, philosophical belief, or religion. This extends to "equal treatment" between part-time and full-time employees, and those on fixed-term versus indefinite-term contracts. Any breach of these provisions can lead to claims for compensation of up to four months' wages, in addition to other rights the employee may have been deprived of.

Employment Contract Typologies

Turkish law defaults to the indefinite-term employment contract. Fixed-term contracts are restricted and can only be established for work that has a predetermined end date or is related to a specific project. Renewing a fixed-term contract without a valid, objective reason converts it into an indefinite-term contract, entitling the employee to greater job security and severance benefits.

A trial (probation) period of up to two months may be included in the contract, during which either party may terminate the relationship without notice or severance pay. Collective bargaining agreements can extend this period to four months.

| Contract Type | Description | Statutory Requirement |

| Indefinite-Term | Default permanent contract | Must be in writing if >1 year |

| Fixed-Term | Project or time-based | Requires objective justification |

| Part-Time | Reduced hours | Must not discriminate vs full-time |

| Remote (Telework) | Work performed outside the office | Must specify conditions and tools |

| On-Call | Work upon employer's request | Governed by Article 14 |

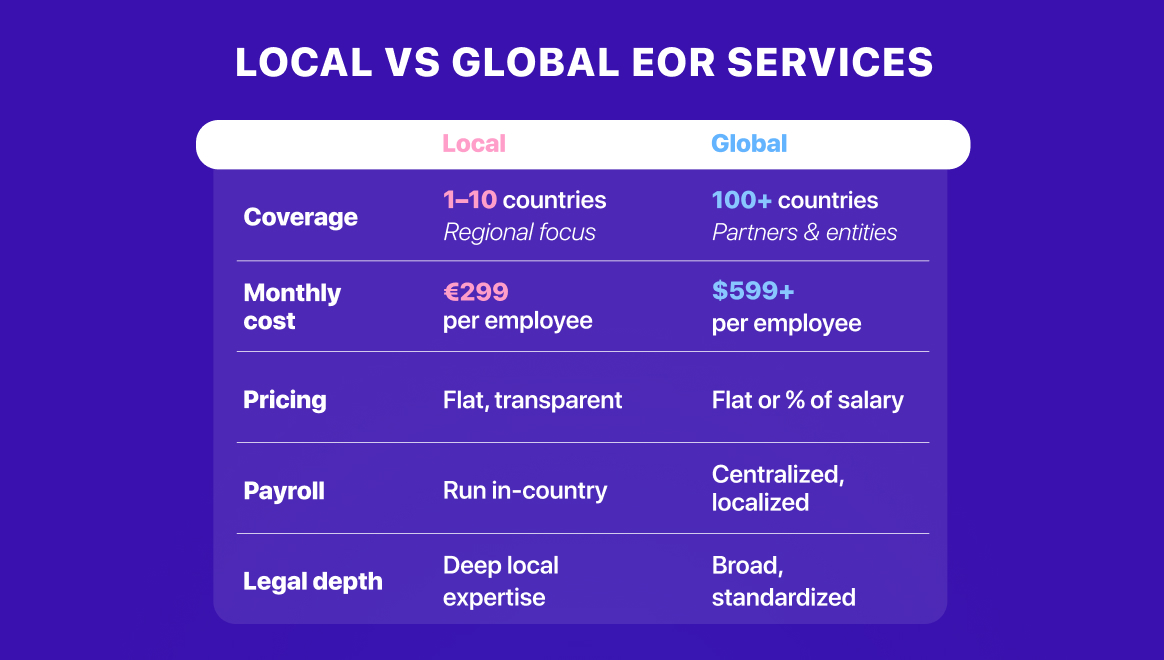

Comparative Analysis: Local vs. Global Employer of Record (EOR) Models

The selection of an EOR provider in Turkey involves choosing between two fundamentally different business models: the wholly-owned entity model and the aggregator (partner-network) model. This choice has deep implications for compliance, communication speed, and cost-efficiency.

The Owned-Entity Model (e.g., Deel, Remote, Multiplier)

Global platforms that own their local Turkish entities, such as Deel, Remote, and Multiplier, provide a unified experience. These providers have established their own legal infrastructure in Istanbul or Ankara, registered with the SGK, and hold local tax IDs.

The primary advantage of the owned-entity model is the elimination of the "middleman" risk. Communication is direct between the client and the provider's local experts, reducing the "game of telephone" common in aggregator models. Furthermore, data security and intellectual property (IP) protection are enhanced because sensitive employee data and IP transfers do not pass through third-party vendors. Remote, for instance, utilizes "Remote IP Guard" to ensure that the maximum possible protection for IP are maintained according to Turkish law.

The Aggregator Model (e.g., Papaya Global, Oyster HR, Lano)

Aggregators rely on a network of in-country partners to facilitate employment. While this model allows for rapid global coverage, it can lead to inconsistent service levels and fragmented workflows. In Turkey, an aggregator might partner with a local boutique firm to handle SGK filings and payroll.

The aggregator model often carries higher hidden costs, as both the global platform and the local partner charge their own fees. Communication delays are more common, as queries regarding specific Turkish regulations must be relayed to the local partner, which can take days rather than hours. Additionally, aggregators have less control over the employee experience, as the local partners' onboarding processes and benefit offerings may differ from the global platform's interface.

Local Boutique Providers (e.g., Team Up, CottGroup, FMC Group)

Local and regional specialists focus specifically on Turkey and neighboring markets like the Caucasus and MENA. Providers like Team Up, CottGroup, and FMC Group emphasize their hyper-local expertise and direct relationships with the Turkish Revenue Administration (GIB) and SGK.

Local boutiques often offer more competitive flat-rate pricing, as they do not have the high overhead of maintaining a global tech stack. They are frequently better equipped to handle complex Turkish-specific issues, such as collective bargaining agreements, specialized industry-wide funds, and hyper-local benefits like private health insurance plans that are tailored to the Turkish medical system.

| Provider Type | Examples | Key Strengths | Primary Risks |

| Owned Global | Deel, Remote, Multiplier | Standardized tech, direct liability, IP protection | Higher pricing, potentially rigid local benefits |

| Global Aggregator | Papaya Global, Oyster | Rapid multi-country hiring, unified reporting | Third-party risk, communication delays, and higher fees |

| Local/Regional | Team Up, CottGroup, FMC | Deep regulatory knowledge, bilingual support, flat-rate fees | Limited global presence, less advanced automation |

Financial Compliance: Payroll, Taxation, and Social Security

Turkish payroll is characterized by a significant gap between gross and net salary, driven by a progressive income tax system and mandatory social security contributions.

The Statutory Contribution Framework

Both the employer and the employee are required to contribute to the SGK system. These contributions cover retirement, disability, health insurance, and unemployment benefits. The standard employer contribution rate is approximately 20.5% to 22.5% of the gross salary, which includes a 2% contribution to the Unemployment Insurance Fund.

Employers may benefit from a 5-percentage-point discount on their social security contributions if they meet specific conditions, such as having no outstanding debt to the SGK and submitting their declarations on time.

| Contribution Type | Employer Rate (Standard) | Employee Rate |

| Social Security (SGK) | 20.5% – 20.75% | 14.0% |

| Unemployment Insurance | 2.0% | 1.0% |

| Income Tax | N/A (Withholding Agent) | 15% – 40% (Progressive) |

| Stamp Tax | N/A (Calculated on Gross) | 0.759% |

| Total Mandatory | ~22.5% – 22.75% | ~15% + Income Tax |

Note: The "Total Social Security" rate for employers is often cited as 20.5%, which, when combined with 2% unemployment insurance, results in a 22.5% total.

Progressive Income Tax Brackets

Turkey utilizes a progressive income tax system where the tax rate increases as the employee's cumulative annual taxable income crosses certain thresholds. Taxable income is calculated by deducting the employee's share of social security and unemployment insurance from their gross salary.

| Estimated 2026 Tax Brackets (TRY) | Tax Rate |

| 0 – 190,000 | 15% |

| 190,001 – 400,000 | 20% |

| 400,001 – 1,500,000 | 27% |

| 1,500,001 – 5,300,000 | 35% |

| 5,300,001 and above | 40% |

Minimum wage earners are generally exempt from income tax and stamp tax on the portion of their income equivalent to the minimum wage.

The 2026 Social Security Reforms (Omnibus Law No. 7566)

Beginning January 1, 2026, Turkey is implementing significant social security reforms that will increase the financial burden on employers and high-earning employees. These changes were enacted via Law No. 7566 and published in the Official Gazette in late 2025.

Increasing the Social Security Ceiling

A major change is the adjustment of the "monthly earnings ceiling" for social security contributions. Historically, the maximum monthly income subject to SGK premiums was 7.5 times the monthly minimum wage. Starting in 2026, this ceiling will increase to 9.0 times the minimum wage.

This reform disproportionately impacts the tech and professional services sectors, where salaries often exceed the previous 7.5x cap. Employers hiring senior talent will see their mandatory social security costs rise as a larger portion of the high gross salaries becomes subject to the ~22.5% employer premium.

The Supplementary Retirement System (TES)

In the second quarter of 2026, the Turkish government plans to launch the Supplementary Retirement System (Tamamlayıcı Emeklilik Sistemi, or TES), replacing the existing Automatic Enrollment System (OKS).

Unlike the current OKS, which is an employee-funded model where employers simply facilitate the deduction, TES will require mandatory employer contributions. Current proposals suggest that employers will be required to contribute 2.0% of the employee's covered pay to an individual TES account. Employees will contribute 3.0%, and the government will provide a 1.0% contribution. This change represents a new, direct labor cost for every employee hired in Turkey.

| Feature | Current OKS (2025) | Proposed TES (2026 Q2) |

| Employer Contribution | 0% (facilitation only) | 2.0% of pay |

| Employee Contribution | 3.0% (opt-out possible) | 3.0% (opt-out unclear) |

| Government Support | 30% of employee contribution | 1.0% of covered pay |

| Enrollment | Auto-enroll if <45 years old | Mandatory for all |

Adjusted Contribution Rates and Incentives

Law No. 7566 also increases the employer's share for long-term insurance branches (invalidity, old-age, and death) from 11% to 12%, raising the total social security premium ratio accordingly. Furthermore, the Treasury-funded employer discount for non-manufacturing companies is being reduced from 4 percentage points to 2 percentage points. Manufacturing companies (NACE Code Section C) will retain their 5-percentage-point discount through the end of 2026.

Statutory Benefits and Local Market "Perks"

In Turkey, the compensation package is traditionally bolstered by a range of allowances and benefits that are either mandatory or culturally expected to attract top talent.

Meal and Transportation Allowances

Meal cards (such as Sodexo, Multinet, or Edenred) are ubiquitous in the Turkish professional market. Employers can provide a daily meal allowance that is exempt from income tax and social security premiums up to a statutory limit. For 2026, the projected daily income tax exemption for meal allowances provided via cards/vouchers is set at approximately 300.00 TRY to 331.10 TRY (including VAT).

Similarly, transportation allowances are common for employees who do not benefit from a company shuttle or vehicle. The 2026 projected daily income tax exemption for transportation cards is 160.00 TRY. These benefits are highly tax-efficient, as they increase the employee's net take-home pay without increasing the employer's tax or SGK burden.

Annual and Special Leave Entitlements

Paid annual leave is mandatory and increases based on the employee's tenure.

| Years of Service | Minimum Annual Leave Days |

| 1 – 5 years | 14 days |

| 5 – 15 years | 20 days |

| 15+ years | 26 days |

Employees under 18 or over 50 years of age are entitled to a minimum of 20 days of leave regardless of tenure.

Other mandatory leaves include:

- Maternity Leave: 16 weeks (8 before, 8 after birth), paid by the SGK.

- Paternity Leave: 5 days paid by the employer.

- Sick Leave: Covered by the SGK after the 2nd day, typically at 66.7% of wages.

- Marriage and Bereavement Leave: 3 days of paid leave.

- Military Leave: Up to 90 days for training/statutory obligations (excluding compulsory service).

Private Health Insurance

While public healthcare is available through SGK, most competitive employers offer private health insurance (PHI). PHI plans typically start from approximately €49 per employee per month and provide access to private hospitals and English-speaking doctors. Offering PHI is considered a "best practice" for remote-first companies to ensure local employees feel valued and protected.

Termination, Severance, and Notice Periods

Turkish labor law is strongly protective of the employee, making termination a process that requires meticulous documentation and adherence to statutory timelines.

Notice Periods and Pay

When terminating an indefinite-term contract without "just cause," both the employer and the employee must provide advance notice. The notice period depends on the length of service.

| Tenure | Notice Period |

| 0 – 6 months | 2 weeks |

| 6 months – 1.5 years | 4 weeks |

| 1.5 years – 3 years | 6 weeks |

| 3+ years | 8 weeks |

If an employer fails to provide the notice period, they must pay "notice pay" (ihbar tazminatı) equivalent to the employee's salary for that period.

Severance Pay (Kıdem Tazminatı)

Severance pay is a critical worker right in Turkey, regulated by Article 14 of the former Labor Law No. 1475 (which remains in effect for this purpose). Employees who have worked for at least one year are entitled to severance pay if they are terminated by the employer without a valid "just cause" (e.g., redundancy) or if they resign for a "justified reason" (e.g., non-payment of wages, unsafe conditions).

Severance is calculated as one month's last gross salary for each full year of service. The calculation must include not only the base salary but also all "continuous monetary and measurable benefits" such as meal allowances and regular bonuses.

The government sets a "severance pay ceiling" (tavan) that limits the maximum amount payable per year of service, updated every six months.

| Period | Severance Pay Ceiling (TRY) |

| Jan – June 2025 | 46,655.43 |

| July – Dec 2025 | 53,919.68 |

| 2026 (Projected) | ~65,000.00 |

Termination for "Just Cause"

Under Article 25 of Law No. 4857, employers can dismiss an employee immediately without notice or severance pay for "just cause," which includes serious misconduct, acts of dishonesty, or health reasons that prevent performance. However, the burden of proof lies entirely with the employer, and Turkish labor courts often reinstate employees if the justification is deemed insufficient.

Temporary Employment and the "Article 7" Risk

A unique challenge for EORs in Turkey is the regulation of "Temporary Employment Relationships" under Article 7 of the Labor Law.

Limits on Secondment and Labor Lending

Article 7 was amended by Law No. 6715 to regulate how employers can "lend" their employees to other firms. A temporary employment relationship can be established within a holding company or between affiliated workplaces for a maximum of four months, renewable twice (totaling eight months).

For EORs, this presents a legal nuance. If the relationship is viewed strictly as "labor lending," it could theoretically be subject to these time limits. To avoid this, reputable EORs structure their services as "service outsourcing" or "project-based management" rather than simple labor supply. The EOR must handle substantive HR and business activities, managing working conditions, leaves, and specific project functions—to move beyond the "temporary worker" label and maintain a long-term, compliant relationship.

Risks of Misclassification and Permanent Establishment

Many foreign firms attempt to bypass EORs or local entities by hiring Turkish talent as "independent contractors". While seemingly cost-effective, this strategy carries significant financial and legal risk.

The Employee-Contractor Distinction

Turkish authorities use several tests to determine if a worker is a contractor or a misclassified employee :

- Control and Dependency: Does the employer dictate the hours, location, and tools? If yes, they are likely an employee.

- Integration: Is the worker integrated into the company hierarchy (e.g., attending all-hands meetings)?

- Economic Dependency: Is the worker financially dependent on a single client?

If misclassified, the employer may be forced to pay backdated SGK contributions (up to 5 years), unpaid taxes with interest, and retroactive severance pay. Furthermore, misclassified contractors may claim the same job security rights as employees, leading to expensive lawsuits.

Permanent Establishment (PE) Risk

Hiring a direct employee or a heavily managed contractor in Turkey can create a "Permanent Establishment" for the foreign company. This triggers an obligation to pay Turkish corporate income tax on profits generated within the country. An EOR acts as the legal employer, effectively creating a barrier that prevents the foreign parent from establishing a taxable nexus in Turkey.

Licensing and Private Employment Agencies (İŞKUR)

The legal operation of an EOR in Turkey is tied to the concept of the Private Employment Agency (Özel İstihdam Bürosu). Under Law No. 4904, these agencies must be permitted by İŞKUR (the Turkish Employment Agency) to carry out recruitment brokerage and human resources services.

Licensing requires the agency to maintain capital adequacy and provide a guarantee letter (e.g., ~51,168 TL in 2019, adjusted annually). It is strictly forbidden for these agencies to charge fees to job seekers; they must only be compensated by the employer. For a foreign company, verifying that an EOR holds a valid İŞKUR license is a fundamental part of the due diligence process.

Navigating the Work Permit Landscape

Hiring foreign talent (expats) to work in Turkey requires a work permit issued by the Ministry of Labor and Social Security.

The 5-to-1 Ratio and Financial Criteria

A major hurdle for sponsoring work permits is the requirement to maintain a ratio of five Turkish employees for every one foreign employee. Additionally, the employer must meet financial criteria, such as a minimum paid-in capital of 100,000 TRY or annual sales of at least 800,000 TRY.

EORs can simplify this process by using their existing large workforce to satisfy the 5-to-1 ratio, allowing smaller foreign firms to hire specialized expat talent without having to hire five local employees first.

Work Permit Categories

| Permit Type | Purpose | Key Condition |

| Temporary | Standard employment | 1-year initial validity |

| Permanent | Long-term residents | 8 years of legal work history |

| Independent | Entrepreneurs | 5 years of residence required |

| Turquoise Card | Highly skilled talent | Permanent work/residence rights |

Strategic Considerations for Provider Selection

Choosing the right EOR partner in Turkey depends on the scale of hiring, the complexity of the roles, and the long-term vision for the Turkish market.

Decision Checklist for HR Leaders

- Wholly-Owned vs. Aggregator: Does the provider own the Turkish entity? Ownership guarantees direct responsibility for SGK audits and faster communication.

- Pricing Structure: Is the pricing a flat fee (e.g., ~$199–$599/month) or a percentage of payroll (e.g., 10–15%)? Flat fees are more predictable as salaries grow.

- Bilingual Support: Does the provider have local HR and legal experts who speak both Turkish and English? This is essential for smooth onboarding and resolving local disputes.

- 2026 Readiness: Is the provider prepared for the 9x SGK ceiling and the TES retirement system implementation? Systems must be ready to adjust calculations by January 1, 2026.

- Scalability: Can the provider support a transition from EOR to a local entity if the team grows beyond 20–30 employees?

Conclusion: Synthesis and Future Outlook

The Turkish employment market is entering a phase of heightened regulatory complexity. The convergence of inflation-driven minimum wage hikes, the 2026 social security overhaul, and the expansion of the SGK premium ceiling makes the Employer of Record more than just a convenience; it is a strategic necessity for risk mitigation.

For most organizations, the owned-entity global model (e.g., Deel, Remote) provides the highest level of IP protection and liability control.

However, for startups and SMEs targeting the region specifically, local boutiques like Team Up offer significant cost advantages and more tailored bilingual support.

Regardless of the chosen model, the objective remains the same: ensuring that talent in Istanbul, Ankara, or Izmir is integrated into the global workforce with the same speed, security, and compliance as any local hire, while shielding the parent organization from the intricate bureaucratic labyrinth of the Turkish labor code.

Frequently asked questions

Best Global EORs: Deel vs. Team Up (Turkey Specific)

While Deel is a global powerhouse, Team Up operates as a specialized regional operator. The choice depends on your scale and need for "high-touch" compliance.

- Deel: Best if you are hiring in 15+ countries and want a single dashboard. Deel owns its entity in Turkey, offering a polished UI but at a premium price (starting at $599/mo). Support is often through a global ticket queue.

- Team Up: Best if Turkey is a strategic hub. As a local specialist, Team Up offers deeper integration with the Turkish "E-Gov" system and lower flat fees. You get direct access to experts who handle local equipment, mandatory health checks, and severance disputes.

Cost Comparison: Local vs. Global EOR (2026)

In 2026, the cost gap has widened. Global EORs often charge a "convenience tax" that can double your management spend.

- Local EOR: Typically a Flat Monthly Fee. Since they have lower overheads in-country, they can offer rates 40-60% lower than global aggregators.

- Global EOR: Usually $599 - $699/mo or a percentage of salary (usually 10-15%).

Compliance Risks Using Global EOR in Turkey

Turkey’s labor system is "document-forward." Using a global platform that lacks deep local roots can trigger specific risks:

- SGK Registration Lag: Contracts must be registered in the SGK portal before work starts. Global platforms often have a 2-4 day lag, technically resulting in "unregistered labor" fines.

- Severance Pay (Kıdem Tazminatı): Turkey has strict rules on severance for employees with 1+ year of tenure. Global platforms sometimes miscalculate these accruals, leading to lawsuits during offboarding.

- Permanent Establishment (PE): If a Global EOR doesn't manage your "Senior Sales Leader" correctly, the Turkish government may claim your company has a taxable "Permanent Establishment" in Turkey, exposing your global revenue to local corporate tax.

EOR vs. Setting Up a Local Entity: Pros & Cons

Choosing between an EOR and a subsidiary (Ltd. Şti.) is a matter of long-term vision vs. immediate speed.

| Feature | Employer of Record (EOR) | Setting Up a Local Entity |

| Setup Time | 2–5 Days | 4–10 Weeks |

| Upfront Cost | Zero | $3,000 – $8,000 (Legal/Notary) |

| Compliance | Managed by EOR | You are 100% Liable |

| Control | Operational Only | Full Legal & Brand Control |

| Best For | Testing markets / Teams < 10 | Permanent Hubs / Teams > 15 |

.svg)