How does an Employer of Record (EOR) manage payroll taxes in Georgia

TL;DR: Payroll taxes and EOR in Georgia

Here’s the short version for decision-makers:

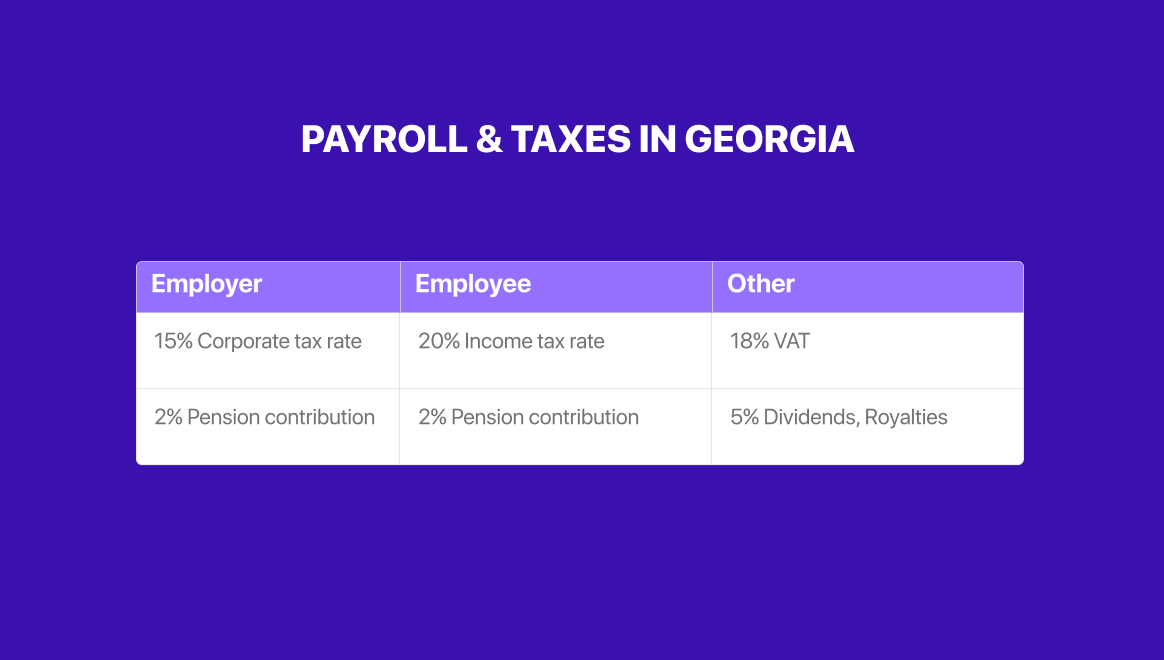

- Payroll taxes in Georgia: Employees pay a flat 20% personal income tax, plus 2% pension and 2% social security. Employers also contribute 2% pension and 2% social security.

- PEO vs EOR: PEOs can manage payroll and benefits, but your company retains legal liability. EORs become the legal employer, handling payroll, taxes, and statutory compliance.

- EOR advantages: Simplifies payroll, ensures compliance, reduces legal risk, and allows hiring without a local entity.

- Timing: Taxes and contributions are paid monthly; filings are due by the 15th of the following month.

- Operational benefits: EORs manage equipment, remote work setup, and employee benefits, using payroll systems to ensure accuracy.

Bottom line: If you’re hiring in Georgia without a local entity or want full compliance with minimal risk, an EOR is the way to go.

Introduction

Hiring in Georgia sounds simple on paper: post a job, find someone talented, pay them.

But in reality, Payroll taxes will quietly turn that “simple” into a paperwork nightmare if you’re not careful. Income tax, social contributions, statutory deductions… It’s a lot to track, especially if your company is based abroad.

Enter the Employer of Record (EOR). The EOR becomes the legal employer for your Georgian hires, handling contracts, payroll, statutory benefits, and compliance.

Basically, we take on the boring-but-critical stuff so you can focus on managing the team instead of deciphering tax codes and filing forms in a language you probably don’t speak.

In this article, we’ll break down:

- How payroll taxes in Georgia actually work for employees

- What an EOR does to calculate, withhold, and file taxes correctly

- Why outsourcing payroll compliance via an EOR can save your team time, money, and headaches

Let’s get into it.

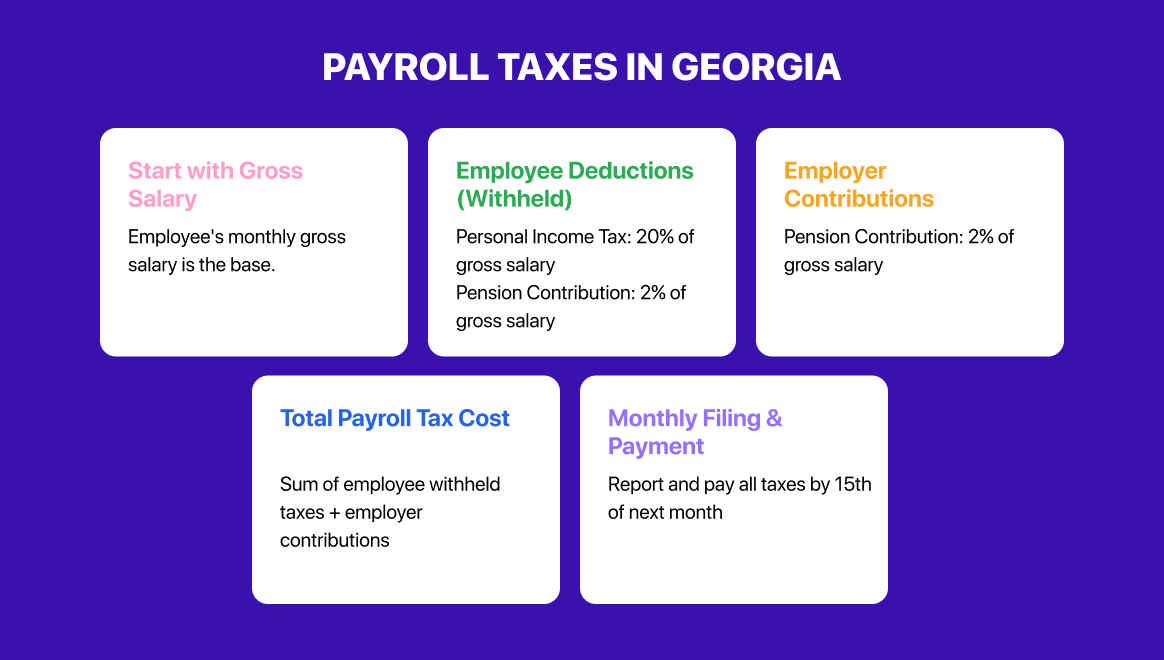

Overview of payroll taxes in Georgia

If you think hiring in Georgia is as simple as posting a job and transferring a salary, welcome to the world of payroll taxes, where the numbers sneak up on you faster than your first cup of Georgian wine.

Get them wrong, and you’re looking at fines, audits, and some very unhappy finance teams.

Personal Income Tax (PIT) in Georgia

Here’s the deal: employees pay 20% flat personal income tax, which your company must withhold and remit. Sounds straightforward, right? But then there are pension and social security contributions, which both employees and employers pay, 2% each. That’s another 4% you need to account for.

Employee vs employer contributions:

- Employee: 20% PIT + 2% pension + 2% social security

- Employer: 2% pension + 2% social security

The key takeaway? Payroll taxes in Georgia aren’t just a line on a spreadsheet, they directly impact take-home pay, your company’s bottom line, and compliance risk.

Mess up, and the Revenue Service isn’t exactly going to send a friendly postcard.

Payroll Taxes vs Personal Income Tax

Let’s clear the fog:

- Personal Income Tax (PIT) is the 20% deducted from the employee’s gross salary.

- Payroll Taxes cover everything else: employer contributions, social security, pension obligations. It’s the full picture of what it costs to legally employ someone in Georgia.

Think of PIT as the slice of salary that disappears from your employee’s bank account, while payroll taxes are the “bonus slice” that your company has to cover on top.

Quick reference table

| Tax Type | Rate | Paid By | Notes |

| Personal Income Tax (PIT) | 20% | Employee | Deducted at source, remitted by employer |

| Employer Pension Contribution | 2% | Employer | Paid directly to pension account |

| Employer Social Security | 2% | Employer | Paid to state social security system |

| Employee Pension Contribution | 2% | Employee | Deducted from salary, goes to pension |

| Employee Social Security | 2% | Employee | Deducted from salary, remitted to social system |

If you’re a foreign company remote hiring in Georgia, managing these payroll taxes correctly is mission-critical. And here’s where an Employer of Record (EOR) comes in handy. The EOR provider in Georgia becomes the legal employer, handles PIT, social contributions, and compliance filings, and frees you from the headache of figuring out Georgian labor law while you focus on growing your team.

How an EOR manages payroll taxes in Georgia

If you’re hiring in Georgia without a local entity, the Employer of Record (EOR) is your legal safety net. The EOR becomes the official employer, which means they’re responsible for withholding, calculating, and filing all payroll taxes while you manage the team’s day-to-day work. Think of it as handing the complex, compliance-heavy stuff to someone who actually knows what they’re doing.

Monthly payroll process managed by the EOR

The EOR oversees the entire monthly payroll cycle, which includes:

- Salary Calculation: Determining gross salaries based on employment agreements.

- Tax Withholding: Deducting the 20% personal income tax from employees' gross salaries.

- Pension Contributions: Managing both employee and employer contributions to the pension scheme, each at 2% of the employee's salary.

- Social Security Contributions: Handling the 2% contribution from both the employee and employer to the state social security system.

By centralizing these processes, the EOR ensures that all statutory obligations are met without your direct involvement.

Employer-only contributions and tax calculations

On top of employee deductions, the EOR covers the employer’s portion of mandatory contributions:

- Employer pension contribution: 2% of gross salary

- Employer social security contribution: 2% of gross salary

These are remitted alongside employee taxes, ensuring full compliance with Georgian labor and tax law.

Technology and compliance

To maintain accuracy and compliance, EORs utilize advanced payroll software systems. These systems:

- Automate Calculations: Ensuring precise deductions and contributions.

- Track Deadlines: Reminding of upcoming tax filing and payment due dates.

- Generate Reports: Providing detailed payroll reports for transparency and record-keeping.

By leveraging technology, EORs minimize errors and streamline the payroll process.

Payroll tax calculation and reporting in Georgia

If you think payroll in Georgia is just sending salaries and calling it a day, think again.

Between personal income tax, pension contributions, and social security, there’s a lot to track, and mistakes can be costly.

Here’s how Employer of Record (EOR) services manage it all so you don’t have to.

How payroll taxes are calculated

In Georgia, payroll taxes involve a combination of personal income tax (PIT) and pension contributions:

- Personal Income Tax (PIT): 20% of the employee’s gross salary.

- Employee Pension Contribution: 2% of gross salary.

- Employer Pension Contribution: 2% of gross salary.

Example:

An employee earns GEL 3,000 per month. Payroll tax calculations would look like this:

- PIT (20%): 3,000 × 20% = GEL 600

- Employee Pension (2%): 3,000 × 2% = GEL 60

- Employer Pension (2%): 3,000 × 2% = GEL 60

Total deductions from the employee: GEL 600 + GEL 60 = GEL 660

Total cost to the employer: 3,000 + 60 = GEL 3,060

This ensures compliance with Georgian tax law while keeping the process transparent for both the company and the employee.

Timing of payroll tax payments and filings

- Payment deadlines: All payroll taxes and contributions must be paid to the Revenue Service by the last working day of the month.

- Filing deadlines: Employers must submit monthly payroll tax declarations by the 15th of the following month.

Missing these deadlines can result in penalties and interest, making timely payroll management essential.

Employer responsibilities

Even when using a PEO or other HR support, the legal responsibility for registration and monthly declarations falls on the employer. With an EOR, however:

- The EOR registers your employees with tax authorities.

- Calculates taxes and contributions correctly.

- Submits monthly declarations and ensures filings are accurate and on time.

This means your company can focus on managing employees while the EOR handles all tax registration, calculation, and reporting obligations.

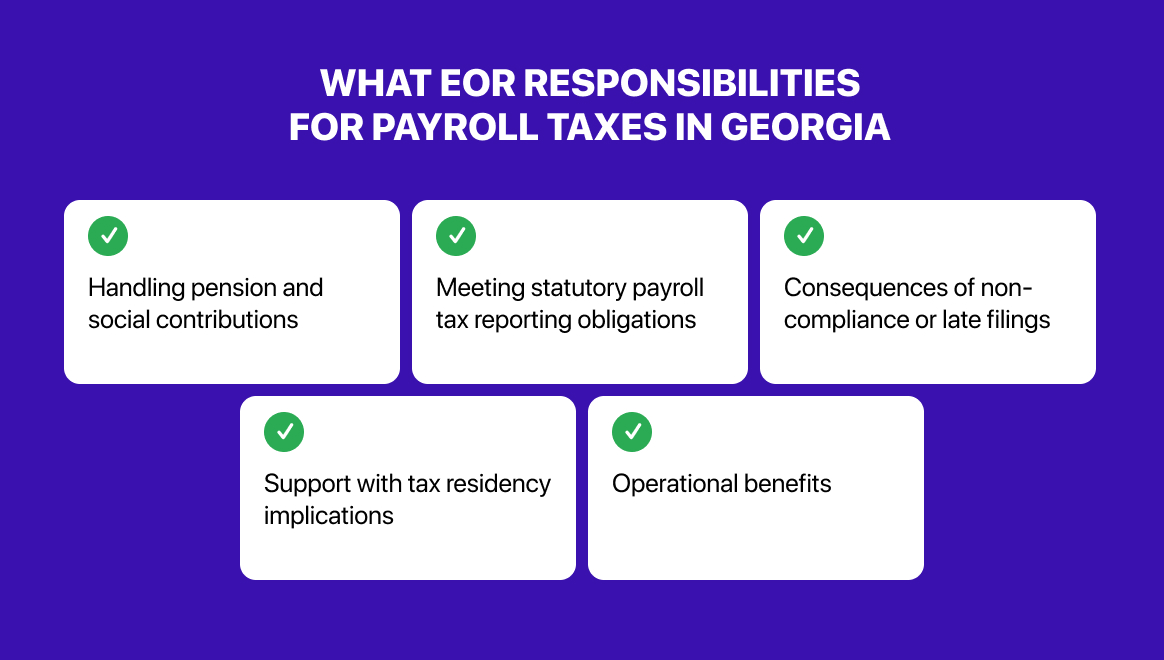

What are the additional responsibilities of an EOR related to payroll taxes in Georgia?

When you hire through an Employer of Record (EOR) in Georgia, payroll taxes are just the starting point. The EOR takes on a broader set of responsibilities that keep your company compliant and employees properly accounted for. Here’s a detailed look at what that entails.

Handling pension and social contributions

An EOR manages both employee and employer contributions to Georgia’s social security and pension system:

- Employee contributions: Deducted from the salary (typically 2% for pension and 2% for social security).

- Employer contributions: Paid on top of the gross salary (2% for pension, 2% for social security).

By managing these accurately, the EOR ensures that employees’ future benefits are secured and your company remains fully compliant with local law.

Meeting statutory payroll tax reporting obligations

Beyond just paying salaries, the EOR handles mandatory reporting to Georgian authorities, including:

- Monthly payroll tax declarations

- Filing of social insurance and pension contributions

- Ensuring all reports are submitted by the statutory deadlines

This removes the risk of penalties for late or incorrect filings and keeps your company in good standing with the Revenue Service.

Consequences of non-compliance or late filings

Getting payroll taxes wrong in Georgia isn’t just an inconvenience, penalties can be significant:

- Fines for late payments or miscalculations

- Interest on unpaid contributions

- Potential audits that require retroactive corrections and administrative effort

By using an EOR, your company shifts these risks to the provider, reducing legal exposure and administrative burden.

Support with tax residency implications

Employees hired through an EOR may have residency considerations, especially if they split time between Georgia and another country. The EOR can:

- Assess tax residency status for employees

- Ensure correct withholding and reporting based on residency rules

- Advise on compliance with cross-border payroll regulations

This is particularly important for multinational companies managing hybrid or remote teams.

Operational benefits

In addition to compliance, EORs simplify team management:

- They integrate payroll processing with employee management systems, streamlining reporting and recordkeeping.

- They provide operational support for managing multiple hires efficiently.

Benefits of using an EOR for payroll tax management in Georgia

Hiring in Georgia as a foreign company comes with a few headaches you don’t see on the job board: payroll taxes, social contributions, statutory reporting, and the dreaded local entity setup. This is exactly where an Employer of Record (EOR) becomes more than just a convenience; it’s a strategic advantage.

Simplification and risk reduction

An EOR handles all payroll calculations, tax withholdings, and social contributions on your behalf. That means no guessing whether you’ve applied the 20% personal income tax correctly, or if the 2% pension contributions for both employee and employer are properly calculated.

Compliance errors? Penalties? Audits? Handled by the EOR, not you. This significantly reduces operational risk for foreign employers entering the Georgian market.

Avoidance of local entity setup

Setting up a local entity in Georgia isn’t impossible, but it takes time, capital, and bureaucracy. EOR services eliminate this requirement entirely. Your company can hire employees legally and compliantly without registering a Georgian subsidiary, allowing you to test the market or scale teams quickly..

Streamlined payroll compliance and tax payment

EORs manage monthly payroll cycles, including:

- Salary calculation and payment

- Income tax withholding (20% flat PIT)

- Employee and employer pension contributions (2% each)

- Monthly filings with Georgian tax authorities

The outcome is predictable, accurate payroll, with a single invoice covering all the costs to use EOR in Georgia, making budgeting and finance management straightforward.

Access to local expertise and software

EORs bring deep local knowledge of Georgian labor law and payroll regulations, combined with dedicated payroll software. This ensures that:

- Calculations are accurate and compliant

- Reporting is timely and meets regulatory requirements

- Any changes in labor law are incorporated immediately

Essentially, you get the expertise of a local HR and payroll team without the overhead of hiring one yourself

Conclusion

Managing payroll taxes, social contributions, and statutory benefits in Georgia doesn’t have to be complicated or risky

This is exactly why an Employer of Record (EOR) matters. An EOR acts as the legal employer of your team: they issue contracts, calculate payroll, withhold taxes, pay social contributions, and file all the necessary reports. You still manage your team’s day-to-day work, but the compliance and legal liability in Georgia sit with the EOR.

With TeamUp’s Employer of Record (EOR) services, you can hire employees legally, ensure full compliance, and avoid fines or back-pay claims, all without setting up a local entity.

Take the next step for your business: schedule a meeting with our Georgia EOR experts. We’ll:

- Walk you through compliant payroll management

- Show you how to streamline taxes, social contributions, and filings

- Help you hire employees quickly and legally without local entity setup

- Provide a custom quote and plan tailored to your hiring goals

Click below to book your meeting and get your Georgia team onboarded with confidence.

Frequently Asked Questions

How to record payroll tax expenses?

Payroll tax expenses should be recorded as part of your company’s employment costs. In Georgia, this typically includes income tax withheld from employees’ salaries and employer contributions to the Pension Fund. When working with an EOR, these expenses are consolidated into a monthly invoice, simplifying your accounting.

What payroll taxes do employers pay in Georgia?

Employers in Georgia are responsible for contributions to the Pension Fund, which is 2% from the employer, 2% from the employee, and 2% from the government. The employer must also withhold a flat 20% personal income tax from employee salaries and remit it to the authorities.

What is the difference between EOR and employee?

An employee is directly hired and legally employed by your company, which assumes all payroll, tax, and compliance responsibilities. An EOR, on the other hand, acts as the legal employer on your behalf. The EOR manages contracts, payroll, and taxes, while the employee still works for your company operationally.

Do employers pay state and local payroll taxes?

No. Georgia has a centralized tax system, which means there are no additional state or local payroll taxes. Payroll obligations are limited to national income tax and mandatory pension contributions.

Which payroll taxes must an EOR withhold in Georgia?

An EOR in Georgia withholds:

- 20% personal income tax from employee salaries

- 2% employee pension contributions The EOR also ensures the employer’s 2% pension contribution is paid, along with the state’s matching contribution.

How does an EOR calculate employer contributions in Georgia?

The EOR calculates contributions based on gross salary:

- 20% income tax withheld from the employee

- 2% employer contribution to the Pension Fund

- 2% employee contribution to the Pension Fund

- 2% state contribution to the Pension Fund (handled by government) This ensures all statutory obligations are met.

What payroll reporting deadlines must an EOR meet in Georgia?

In Georgia, payroll taxes and pension contributions must be reported and paid monthly, usually by the 15th of the following month. An EOR ensures deadlines are met to avoid penalties or interest charges.

Do EORs handle pension and social contributions for Georgian hires?

Yes. The EOR manages both employer and employee contributions to Georgia’s mandatory pension system. While Georgia does not have broad social security contributions like some other countries, the pension scheme is mandatory and fully administered by the EOR.

How does using an EOR affect employee tax residency in Georgia?

Using an EOR does not change an employee’s tax residency. Employees remain subject to Georgian tax residency rules, which are based on time spent in the country (183 days or more in a 12-month period). The EOR ensures taxes are withheld correctly according to Georgian law.

.svg)