Local vs Global Employer of Record (EOR) in India: A Comprehensive Guide

TL;DR

Expanding into a new market is often marketed as a seamless "plug-and-play" experience by most international service providers. However, for a company looking to establish a footprint in the subcontinent, the reality of navigating Employer of Record services in India is more akin to solving a high-stakes puzzle where the rules of the game have just been rewritten. In late 2025 and throughout 2026, the implementation of the Four New Labor Codes has fundamentally altered the compliance landscape in India, making the choice between local direct providers and global aggregators a decision that can either safeguard a company’s future or leave it exposed to systemic risk.

The traditional approach of "corporate fluff", promising global reach without local depth, is the Marmite of the EOR industry. People can smell the lack of expertise from a mile away. In India, honesty is not just the best policy; it is the only way to survive the transition from 29 archaic central laws to a unified, digital-first regulatory framework.

This guide serves as an exhaustive analysis for decision-makers who recognize that hiring in emerging hubs like India requires a nuanced understanding of the Code on Wages, the 50% basic pay rule, and the operational friction of a 48-hour final settlement mandate.

Quick Navigation

- TL;DR

- The 2026 Regulatory Landscape: A Seismic Shift in Indian Labor Law

- The "50% Wage Rule": Financial Implications for Global Employers

- Local vs. Global EOR: The Battle for Accountability

- The "Contractor Trap" and Misclassification Risks

- Operational Friction: The 48-Hour Final Settlement Mandate

- Statutory Benefits and the Cost of Employment

- Regional Nuances: The Shops and Establishments Act

- Financial Transparency: Forex Markups and GST

- Permanent Establishment (PE) and the DTAA

- Strategic Benefits of the EOR Approach in 2026

- Conclusion: The Path Forward for Global Hiring

- Frequently Asked Questions

The 2026 Regulatory Landscape: A Seismic Shift in Indian Labor Law

The transition to the Four New Labor Codes on November 21, 2025, marks the most significant legislative overhaul in India’s labor history since 1947. For any organization utilizing eor services in India, understanding this transition is the first step toward legitimate operation. The government’s objective was to promote formalization and social security, but for the employer, it has introduced a period of unprecedented structural adjustment.

The Consolidation of Archaic Frameworks

The new framework replaces a fragmented system where companies had to comply with nearly 30 different central laws and hundreds of state-level rules. This modernization, aligned with the "Aatmanirbhar Bharat" (Self-Reliant India) initiative, aims to reduce administrative burden while simultaneously strengthening worker protections. The four codes, Wages, Social Security, Industrial Relations, and Occupational Safety, Health and Working Conditions (OSH), now serve as the primary pillars of employment compliance.

| Code | Former Statutes Replaced (Selection) | Core Regulatory Focus |

| Code on Wages, 2019 | Payment of Wages Act (1936), Minimum Wages Act (1948), Payment of Bonus Act (1965), Equal Remuneration Act (1976) | Uniform wage definition, minimum floor wages, timely payment, and bonus eligibility. |

| Code on Social Security, 2020 | EPF Act (1952), ESI Act (1948), Maternity Benefit Act (1961), Payment of Gratuity Act (1972) | Expanded coverage for gig/platform workers and fixed-term employees. |

| Industrial Relations Code, 2020 | Trade Unions Act (1926), Industrial Employment (Standing Orders) Act (1946), Industrial Disputes Act (1947) | Streamlined dispute resolution and higher thresholds for government retrenchment approval. |

| OSHWC Code, 2020 | Factories Act (1948), Contract Labour Act (1970), Inter-State Migrant Workmen Act (1979) | Mandatory appointment letters, health check-ups, and gender-inclusive night shift rules. |

The "50% Wage Rule": Financial Implications for Global Employers

For companies evaluating an employer of record in India, the "50% Wage Rule" is the single most important financial metric to understand. Historically, employers in India kept the "Basic Pay" component of a salary structure as low as possible, often 20% to 35% of the total Cost to Company (CTC), while inflating "Allowances" (like House Rent Allowance, Conveyance, or Special Allowance) to minimize their statutory liabilities.

The Mechanism of the Rule

Under the Code on Wages, the definition of "wages" has been standardized. Now, "Basic Pay," "Dearness Allowance," and "Retaining Allowance" must collectively form at least 50% of the total remuneration. If an employer structures a salary where allowances exceed 50%, the excess portion is "added back" to the wage base for the purpose of calculating statutory benefits like Provident Fund (PF) and Gratuity.

This is not a suggestion; it is a hard cap on salary fragmentation. The intent is to ensure that social security contributions are calculated on a more realistic salary base. For a US-based firm, this means the "all-in" cost of an Indian employee is rising, even if the gross salary remains the same.

The Economic Ripple Effect

The restructuring of salary packets leads to two primary outcomes that HR leaders must manage carefully. First, the employer's contribution to PF and the long-term liability for Gratuity increase by approximately 5% to 15%. Second, because PF is a dual-contribution system, the employee's mandatory deduction also increases, leading to a reduction in their monthly "take-home" pay.

| Component | Old Salary Structure Impact | 2026 Labor Code Impact |

| Basic Pay % | Typically 25% – 35% | Minimum 50% |

| PF Contribution | Calculated on a lower base | Calculated on 50% of CTC |

| Gratuity Liability | Lower (based on a small basic) | Higher (based on 50% basic) |

| Employee Net Pay | Higher monthly cash flow | Lower cash flow, higher retirement savings |

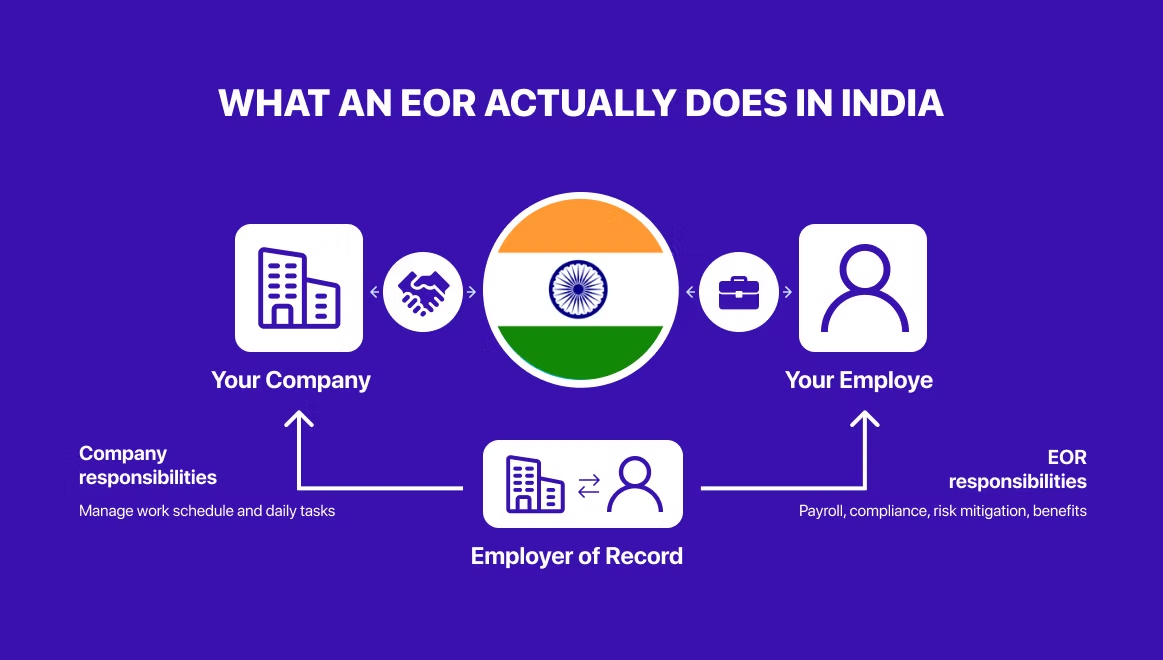

Local vs. Global EOR: The Battle for Accountability

In the burgeoning market for global employer of record services, the choice of provider often boils down to a fundamental question: who actually owns the risk? In the context of India, this distinction is split between global aggregators and local direct EOR partners.

The Aggregator Model: Software with a Partner Shadow

Global aggregators like Deel, Remote, or Multiplier provide a slick, unified interface for hiring in over 100 countries. For a business expanding into multiple regions simultaneously, this centralization is attractive. However, many aggregators do not own an Indian entity. Instead, they operate through a network of local third-party partners.

This creates a "pass-the-blame" risk. When a labor inspector visits or a dispute arises regarding the 2026 codes, the aggregator may lack the direct on-ground authority to resolve the issue. Furthermore, support is often routed through global ticketing systems, which can result in delays during high-stakes compliance crises.

The Direct Model: Regional Ownership and Advisory

Local direct providers, such as Husys or Remunance, own and operate their legal entities in India. For a company focusing specifically on building a team in India, the direct model offers a "legal firewall." Because they are the primary employer, they take direct accountability for all statutory filings, including the complex monthly Tax Deducted at Source (TDS) and Professional Tax (PT) calculations.

Direct providers are also better positioned to provide "founder-level clarity" on local nuances, such as why a software engineer in Karnataka has different leave entitlements than one in Maharashtra.

| Feature | Global Aggregator | Local Direct Provider |

| Accountability | Shared with 3rd parties | Direct legal employer |

| Support Speed | Ticket-based / Global queue | Dedicated local managers |

| Cost Basis | Higher (platform premium) | Lower (no middleman) |

| Expertise | Generalized global focus | Deep local labor code specialization |

The "Contractor Trap" and Misclassification Risks

The ease of hiring an "independent contractor" via a platform often masks a significant compliance nightmare. In India, the distinction between a contractor and an employee is not merely a matter of what you call them in a document; it is a matter of behavioral control.

The Substance Over Form Approach

Indian authorities and courts apply the "Control Test." If your company sets the working hours, provides the equipment, and has the worker performing core business functions, they are legally an employee. Attempting to bypass the 2026 labor framework by using contractor labels creates a substantive compliance failure.

When authorities identify misclassified workers, they apply liabilities retroactively. This includes years of backdated PF contributions, ESI, gratuity accruals, and interest penalties. Furthermore, under the Contract Labour (Regulation and Abolition) Act, the "Principal Employer" (your company) is ultimately liable if the intermediary fails to fulfill wage or welfare obligations.

The Intellectual Property (IP) Vulnerability

Perhaps the most overlooked risk of misclassification is IP ownership. Under Section 17 of the Indian Copyright Act (1957), the author is the first owner of a work unless they are an employee under a "contract of service". For an independent contractor, the IP does not automatically vest with your company unless a valid, written assignment agreement is executed. Without this, a disgruntled former "contractor" could theoretically claim ownership of the code or designs they produced.

| Risk Area | Independent Contractor Model | EOR Employee Model |

| Tax Exposure | High (missing TDS liability) | Low (handled by EOR) |

| Benefit Claims | High (retroactive PF/Bonus) | None (statutory benefits paid) |

| IP Protection | Precarious (requires assignment) | Automatic (contract of service) |

| Legal Status | "Contract for Service" | "Contract of Service" |

Operational Friction: The 48-Hour Final Settlement Mandate

One of the most radical changes in the 2026 labor landscape is the standardization of the Full and Final (FnF) settlement timeline. Historically, when an employee left a company in India, the settlement process could take anywhere from 30 to 45 days, as HR departments reconciled leave encashment, gratuity, and pending expenses.

Section 17(2) of the Code on Wages

Under the new law, all dues must be cleared within two working days of an employee's resignation, dismissal, or retrenchment. This is a significant operational shift that catches many US companies off guard. To meet this window, an EOR must have automated payroll technology capable of real-time calculations.

The challenge is exacerbated in remote working environments. Recovering physical assets, such as laptops or security tokens, becomes a race against the clock. If the settlement is delayed because the asset has not been returned, the employer still faces the risk of penalties under Section 54 for delayed wage payments. A reliable regional EOR partner will have pre-established "Exit Day + 2" processing windows to ensure compliance.

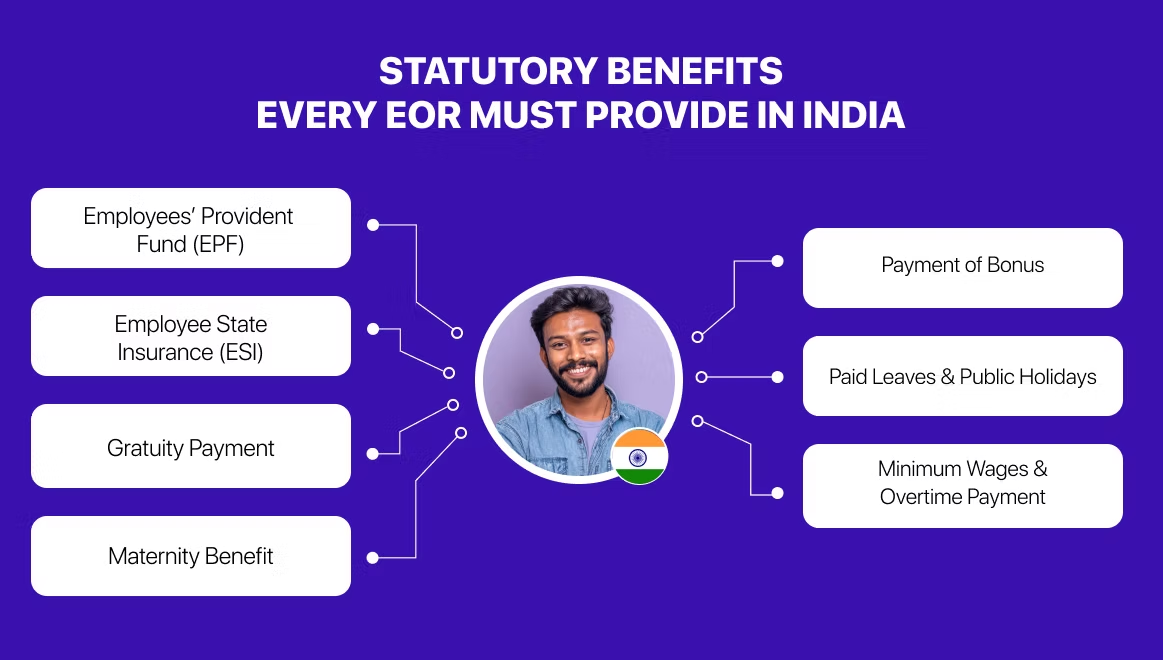

Statutory Benefits and the Cost of Employment

When budgeting for top EOR in India, it is essential to look past the base salary. The "True Employment Cost" is typically 20% to 30% higher than the gross pay once mandatory contributions are factored in.

Mandatory Benefit Breakdown (2026)

| Benefit | Eligibility/Rule | Typical Employer Cost |

| Employees' Provident Fund (EPF) | Mandatory for establishments with 20+ staff. | 12% of Basic + DA |

| Employee State Insurance (ESI) | For employees earning < ₹21,000/month. | 3.25% of Gross Wages |

| Gratuity | Mandatory after 1 year (fixed-term) or 5 years (permanent). | ~4.81% of Basic |

| Statutory Bonus | Mandatory if earning < ₹21,000/month. | 8.33% to 20% of wages |

| Professional Tax | State-specific direct tax on income. | Up to ₹2,500 per year |

The Gratuity Change for Fixed-Term Employees

A critical 2026 nuance is the pro-rata gratuity for Fixed-Term Employment (FTE). Previously, contractors or temporary staff rarely qualified for gratuity. Now, the law mandates parity of benefits. This removes the "cost advantage" of hiring temporary staff over permanent employees, as the FTE must receive the same wages and social security benefits.

Regional Nuances: The Shops and Establishments Act

India is a federal union, and while the four new codes unify central themes, the "Appropriate Government" for daily operational rules is often the state government. Every EOR country operation in India requires registration under the specific Shops and Establishments Act for the state where the employee is located.

Karnataka vs. Maharashtra vs. Delhi

The leave policies, working hours, and even holiday lists vary significantly across major tech hubs. For instance, in Delhi, the daily working hour limit was recently increased to 10 hours (including rest), whereas other states maintain a strict 8-hour day/48-hour week.

| State | Earned Leave (EL) | Casual Leave (CL) | Sick Leave (SL) | Professional Tax (Monthly) |

| Delhi | 15 days/year | 12 days/year | 12 days/year | Not Applicable |

| Karnataka | 1 day per 20 working days | 12 days/year | No Provision | ₹200 (for salary > ₹25k) |

| Maharashtra | 1 day per 20 working days | No Provision | 8 days/year | ₹200 (₹300 in Feb) |

| Uttar Pradesh | 15 days/year | 10 days/year | 15 days/year | Not Applicable |

Financial Transparency: Forex Markups and GST

When choosing between global eor services, the "hidden" financial costs can be as substantial as the service fees. A common practice in the industry is the application of a "Forex Markup".

The Cost of Currency Conversion

Traditional banks and some EOR platforms add a markup of 1.5% to 4% on the mid-market USD-INR exchange rate. This is often hidden; the statement may simply show an "Amount credited" without a breakdown of the conversion loss. For an employer paying a team $50,000 a month, a 3% hidden markup equates to $18,000 per year in additional costs that provide no value to the employee.

Furthermore, GST of 18% is applicable to the service fees charged by the EOR. A transparent provider, in line with Team Up's mission of credibility, will offer flat, predictable pricing with no hidden markups on currency exchange or benefits administration.

Permanent Establishment (PE) and the DTAA

One of the most complex risks for a US company hiring in India is the unintentional creation of a "Permanent Establishment". PE risk arises when a foreign company has a "fixed place of business" or a "dependent agent" habitually concluding contracts on its behalf in India.

Mitigating PE Risk with the EOR Model

Once a PE is established, the host country (India) can tax the US company's global income on the portion attributed to Indian operations. This is an expensive and operationally disruptive scenario. The EOR model is the most effective way to mitigate this risk, as the employees are legally employed by the EOR's local entity, not your foreign corporation.

However, the EOR model is not a "magic shield." If an employee is given the authority to sign contracts or lead strategic business development for the US parent, tax authorities may "look past" the EOR arrangement and conclude that a PE exists. It is critical to align the EOR strategy with guidance from tax counsel.

Strategic Benefits of the EOR Approach in 2026

Despite the complexity of the new labor codes, utilizing an employer of record United States or international model for India offers several strategic advantages for businesses in "emerging hubs."

- Rapid Market Entry: Setting up a local subsidiary (a Private Limited Company) in India can take 3 to 12 months and requires significant capital investment. An EOR allows you to hire in days.

- Compliance Insurance: The EOR assumes the risk of navigating the 2026 transition, ensuring every contract and payroll cycle aligns with the new 50% wage rule and 48-hour settlement mandate.

- Talent Access: By offering fully compliant statutory benefits (PF, ESI, Gratuity, Bonus), you strengthen your employer brand in a highly competitive tech market.

- Scalability: You can easily test pilot teams or scale down without the rigidity and legal complexity of winding down a legal entity.

Conclusion: The Path Forward for Global Hiring

Hiring in India is no longer an exercise in finding the cheapest contractor; it is an exercise in navigating a sophisticated, formalized labor market. The transition to the Four New Labor Codes has removed the "BS" from the employment landscape, forcing transparency in wage structures and speed in exit procedures.

For decision-makers, the choice between local and global EOR services boils down to the depth of expertise you need on the ground. A global platform provides the interface, but a direct local partner provides the "legal firewall" and regional nuance required to thrive in hubs like Bengaluru, Mumbai, and Delhi. By prioritizing action, value, and credibility, your organization can leverage India's massive talent pool without falling into the "contractor trap" or the pitfalls of regulatory non-compliance.

Frequently Asked Questions

1. What is the "50% Wage Rule" and why does it matter?

The 2026 Code on Wages introduces a strict definition of "Wages."

- The Rule: Basic Pay must now constitute at least 50% of the total Cost to Company (CTC).

- The Impact: Historically, companies used low basic pay and high allowances to reduce mandatory Provident Fund (PF) and Gratuity contributions. Under the 2026 rules, this is illegal.

- Local vs. Global: Local EORs (like Team Up) restructured contracts immediately in late 2025. Many Global EORs still use outdated "allowance-heavy" templates, which can lead to back-tax audits and a 10–12% spike in your total employment cost when caught.

2. How do local vs. global EOR prices compare in India?

The pricing gap in India is one of the widest in the world.

- Local EOR (Specialist): Typically charges a flat monthly fee ranging from $99 to $250 per employee. This is often all-inclusive of standard compliance filings.

- Global EOR (Platform): Typically charges $499 to $699 per employee.

- The "Hidden" Tax: Global platforms often charge a percentage of the salary or add-ons for "local benefits" that are actually statutory requirements. For a senior developer in Bangalore, a Global EOR might cost $5,000+ more per year just in management fees.

3. Is there "At-Will" employment in India in 2026?

No. One of the most common mistakes global companies make is assuming they can fire employees as easily as in the US.

- Notice Periods: In India, notice periods are typically 30 to 90 days and are strictly enforced.

- The 48-Hour Rule: Under the 2026 Labor Code, full and final settlement (including all dues, leave encashment, and bonuses) must be paid within 48 hours of an employee's last day.

- The Risk: Global platforms often have a 15–30 day payroll cycle that cannot accommodate a 48-hour final payout, putting you in immediate non-compliance.

4. How does the 2026 Gratuity change affect short-term hires?

- Old Law: Employees were only entitled to Gratuity (a statutory long-term benefit) after 5 years of service.

- New 2026 Law: Fixed-term employees (common in EOR setups) are now entitled to Gratuity on a pro-rata basis after just 1 year of service.

- The Trap: If your EOR budget doesn't accrue for this 1-year gratuity milestone, you will face an unexpected 4.81% (of basic pay) liability at the end of the year.

5. Can I hire contractors instead of full-time employees?

In 2026, the Indian government increased scrutiny on Contractor Misclassification.

- The "Core Activity" Bar: The new Industrial Relations Code generally bars the use of independent contractors for a company's "core business activities."

- The Risk: If you hire a developer as a contractor but they work exclusively for you and use your tools, the authorities may reclassify them as an employee, demanding backdated PF, ESI, and Gratuity. Local EORs default to full employment to protect your Intellectual Property (IP), which in India is much harder to defend with contractors.

.svg)