How does an Employer of Record (EOR) manage payroll taxes in India

TL;DR

India’s payroll system rewards accuracy and punishes guesswork. Here’s what you really need to know:

- Payroll tax rates: Employers contribute about 12% to Provident Fund (PF), 3.25% to Employee State Insurance (ESI), and a small amount toward Professional Tax and Labor Welfare Fund — adding up to roughly 20–22% of gross salary. Employees contribute another 12% (PF) and 0.75% (ESI), plus income tax (TDS) withheld at source.

- EOR’s role: Your Employer of Record (EOR) acts as the legal employer, registering employees with EPFO, ESIC, and the Income Tax Department, calculating payroll taxes, remitting contributions, and issuing bilingual payslips and Form 16.

- Compliance protection: An EOR keeps you 100% compliant by handling PF, ESI, and TDS filings, Form 24Q submissions, and all state-level obligations. No missed challans, no penalties, no legal exposure.

- Why Team Up’s model wins: Most providers charge a percentage of salary. TeamUp uses a flat monthly rate, giving you full compliance, payroll, and employee management without surprise markups, one invoice, one partner, zero red tape.

Hiring in India doesn’t have to be a legal maze. TeamUp makes it clean, compliant, and fast, so you can focus on your team, not tax forms.

Introduction

You can hire anywhere today, but in India, payroll compliance still takes a local expert.

The country’s talent pool is world-class, but so is its paperwork. Between TDS (Tax Deducted at Source), Provident Fund (PF), Employee State Insurance (ESI), and Professional Tax, managing payroll in India is less about math and more about knowing exactly which form to file, when, and with which authority.

Each of these taxes has its own rates, filing schedules, and legal thresholds, and they’re updated more often than most foreign teams realize.

Miss one contribution or file it under the wrong code, and you’re suddenly dealing with penalties, backdated payments, or even employee disputes over net pay.

That’s why more global companies are choosing to hire through an Employer of Record (EOR).

Instead of wrestling with Indian payroll rules, an EOR takes full legal responsibility for compliance, from registering employees with the EPFO and ESIC to calculating TDS, submitting monthly returns, and keeping every payslip audit-ready.

In short, an Employer of Record payroll system in India gives you the reach of a local employer without the red tape of becoming one.

Payroll tax framework in India: Which payroll taxes are paid by employers only

Here’s where payroll in India starts to get real.

Unlike most countries where taxes are centralized, India’s payroll framework is a mix of federal and state-level laws, each with its own rules, rates, and deadlines.

That means what’s mandatory in Mumbai might not apply in Bangalore, and missing one small filing can still cost you nationwide.

Let’s break it down.

1. Income Tax (TDS – Tax Deducted at Source)

This one’s simple in theory but tricky in practice. Employers must deduct income tax at source (TDS) from employee salaries based on India’s progressive income tax slabs (up to 30%).

- Paid by employees, but collected and remitted by employers every month.

- Filed through the Income Tax Department’s portal using Form 24Q.

2. Provident Fund (PF)

Think of this as India’s social security system; it’s mandatory for companies with 20+ employees.

- Employer contribution: 12% of basic salary.

- Employee contribution: 12% of basic salary.

- Filed through the EPFO (Employees’ Provident Fund Organization).

- Covers retirement savings and long-term benefits.

3. Employee State Insurance (ESI)

The ESI scheme provides medical and disability coverage for employees earning under INR 21,000/month.

- Employer contribution: 3.25% of gross salary.

- Employee contribution: 0.75%.

- Managed by the ESIC (Employees’ State Insurance Corporation).

4. Professional Tax (PT)

A small monthly deduction levied by individual state governments, not the center.

- Applies only in certain states (like Maharashtra, Karnataka, Tamil Nadu, and West Bengal).

- The amount varies, usually between INR 200 and INR 2,500 per year.

- Employers are responsible for registering, deducting, and remitting it to the respective State Tax Department.

5. Labor Welfare Fund (LWF)

A minor statutory contribution that funds welfare programs for workers.

- Paid partly by employers, partly by employees (typically INR 10–50 each).

- Frequency varies, monthly, half-yearly, or annually, depending on the state.

Payroll tax breakdown (2025)

| Tax Type | Employer Contribution | Employee Contribution | Paid To |

| Income Tax (TDS) | — | Progressive up to 30% | Income Tax Department |

| Provident Fund (PF) | 12% | 12% | EPFO |

| Employee State Insurance (ESI) | 3.25% | 0.75% | ESIC |

| Professional Tax (PT) | Varies by state | Varies by state | State Tax Department |

| Labor Welfare Fund (LWF) | Nominal (INR 10–50) | Nominal (INR 10–50) | State Welfare Board |

(Sources: Income Tax India Portal, EPFO, ESIC)

So, which payroll taxes are paid by employers only?

Primarily the employer’s share of PF (12%), ESI (3.25%), and their part of the LWF. These are in addition to handling all withholding and remittance obligations for employee-side taxes like TDS and PF deductions.

That’s why most foreign companies rely on an Employer of Record (EOR) to manage payroll in India, because the filing doesn’t end with one portal; it ends with at least four.

Payroll tax vs income tax: The big difference

If you’re hiring in India, you’ll quickly learn that “tax” doesn’t always mean the same thing. Income tax and payroll taxes fall under completely different laws, are paid to different authorities, and serve very different purposes, but both end up on your payroll dashboard every month.

Let’s clear it up.

Income tax (TDS): What employees pay, but you file

Income Tax, or Tax Deducted at Source (TDS), is the tax on an employee’s personal income. The rate is progressive, ranging from 5% up to 30% depending on the salary bracket and whether the employee opts for the new or old tax regime.

Even though it’s the employee’s liability, the employer is legally responsible for:

- Calculating tax according to the employee’s chosen regime.

- Deducting TDS from monthly salaries.

- Depositing it with the Income Tax Department of India by the 7th of the following month.

- Filing quarterly TDS returns (Form 24Q).

- Issuing Form 16 (annual tax certificate) at the end of the financial year.

Miss a single deadline, and both the company and its directors can face penalties or prosecution under the Income Tax Act, 1961.

Payroll taxes: What employers pay to employ legally

Payroll taxes are different; they’re the mandatory social and statutory contributions you owe because you employ someone in India.

They aren’t about an employee’s income; they’re about maintaining compliance with India’s labor and social welfare laws.

Here’s what’s typically included:

| Tax Type | Employer’s Share | Purpose / Authority |

| Provident Fund (PF) | 12% of basic salary | Long-term retirement savings; EPFO |

| Employee State Insurance (ESI) | 3.25% of gross salary | Medical & disability coverage; ESIC |

| Professional Tax (PT) | Varies by state (up to ₹2,500/year) | State-level welfare fund |

| Labour Welfare Fund (LWF) | ₹10–₹50 per employee (state-specific) | Employee welfare initiatives |

Payroll taxes are usually filed and remitted through the EPFO, ESIC, and state government portals. Some states even have their own digital systems, like Maharashtra’s PT portal or Karnataka’s e-Payment gateway.

So, how are payroll taxes different from personal income taxes?

It comes down to who owes the money and why.

| Category | Who Pays | What It Covers | Filed By |

| Income Tax (TDS) | Employee | Personal income liability | Employer (as deductor) |

| Payroll Taxes (PF, ESI, PT, LWF) | Employer (partly shared with employee) | Social security, insurance, and welfare | Employer |

In short, income tax is about the employee’s earnings, while payroll taxes are about the employer’s compliance duties. Yet in both cases, you, the employer, carry the filing and remittance responsibility.

The cost of compliance in context

According to the OECD Global Tax Database, India’s total employer-side payroll contribution burden averages 20–22% of gross salary, compared to an OECD average of 23–25%.

That means India’s labor taxes are competitive, but not forgiving. The laws are strict, multi-layered, and constantly updated, and even a small oversight (like missing a PF challan or ESI return) can result in penalties that wipe out the savings of hiring abroad.

Why global employers use EORs to manage both

When you hire through an Employer of Record (EOR) provider in India, you’re outsourcing both categories of tax, income tax (TDS) and payroll taxes (PF, ESI, PT), to a local compliance specialist.

Your EOR:

- Registers employees with EPFO, ESIC, and state authorities.

- Calculates TDS, PF, and ESI each month.

- Files returns and pays taxes on time.

- Issues bilingual payslips and Form 16 to employees.

- Keeps every record audit-ready for Indian authorities.

Essentially, you get full legal compliance without ever touching a government portal.

How to calculate payroll taxes in India (with example)

If you’ve ever tried to figure out how to compute payroll taxes in India manually, you know it’s not a one-formula job. Between federal deductions, state-specific levies, and different contribution caps, you’re juggling at least five moving parts — each with its own rate and reporting format.

Let’s make it real with an example.

Say you’re hiring a mid-level employee in Bangalore earning a gross monthly salary of ₹100,000. Here’s what happens from the offer letter to the payslip.

Step 1: Start with gross salary

This is the total monthly amount agreed upon before any deductions — ₹100,000.

Step 2: Calculate employee deductions

These are contributions or taxes withheld from the employee’s salary.

| Deduction Type | Rate | Amount (₹) | Notes |

| Provident Fund (PF) | 12% | 12,000 | Mandatory if basic salary ≤ ₹15,000; usually extended voluntarily for higher earners. |

| Employee State Insurance (ESI) | 0.75% | — | Not applicable since ESI covers salaries up to ₹21,000/month. |

| Income Tax (TDS) | Progressive | ~10,000 | Estimated using current tax slabs under the new regime. |

| Professional Tax (PT) | Fixed | 200 | Varies by state; here, Karnataka applies ₹200/month. |

Total Employee Deductions: ₹22,200

So, Net Pay to Employee = ₹100,000 − ₹22,200 = ₹77,800

Step 3: Add employer contributions

Now, let’s see what the employer actually pays.

| Employer Contribution | Rate | Amount (₹) | Paid To |

| Provident Fund (PF) | 12% | 12,000 | EPFO |

| Employee State Insurance (ESI) | 3.25% | — | ESIC |

| Professional Tax (PT) | Fixed | 200 | State Govt (Karnataka) |

| Labor Welfare Fund (LWF) | Fixed | 20 | State Welfare Board |

Total Employer Contributions: ₹12,220

So, Total Employer Cost = ₹100,000 + ₹12,220 = ₹112,220/month.

Gross → Net breakdown (Illustration)

| Category | Rate / Type | Amount (₹) |

| Gross Salary | 100,000 | |

| Employee PF (12%) | Deduction | −12,000 |

| Employee Income Tax (TDS) | Deduction | −10,000 |

| Professional Tax | Deduction | −200 |

| Net Pay (Employee Receives) | 77,800 | |

| Employer PF (12%) | Contribution | +12,000 |

| Employer PT + LWF | Contribution | +220 |

| Total Employer Cost | 112,220 |

Step 4: Review the compliance picture

For every payroll cycle, the employer (or your EOR) must:

- Deposit PF and ESI via government portals (EPFO & ESIC).

- Remit TDS to the Income Tax Department of India by the 7th of the next month.

- File quarterly TDS returns (Form 24Q) and issue Form 16 annually.

- Submit Professional Tax and Labor Welfare Fund payments to the respective state departments.

That’s a lot of moving parts for one salary.

Why it matters

If you’re calculating employer payroll taxes in-house, every one of those filings is your liability, not your accountant’s, not your employee’s.

That’s why companies hiring in India through Team Up’s Employer of Record (EOR) model hand over the entire process: we register, calculate, file, and remit every payroll tax under our local entity.

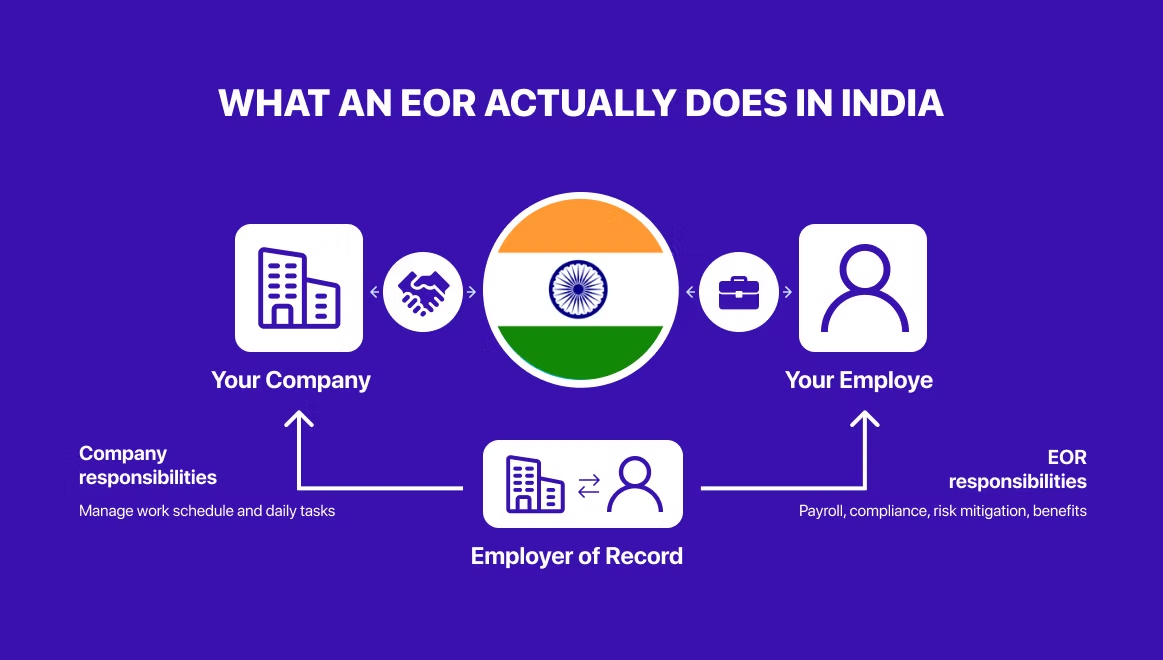

How an Employer of Record (EOR) manages payroll tax compliance

If you’ve ever tried to manage payroll compliance in India on your own, you know it’s less about paying people and more about navigating an alphabet soup of filings, EPFO, ESIC, TDS, PT, and Form 24Q. One missed form, and you’re staring down late fees, mismatched returns, and sleepless nights for your finance team.

That’s why global companies expanding into India turn to an Employer of Record (EOR).

Your EOR becomes the official employer of your team in India — legally recognized by the Employees’ Provident Fund Organisation (EPFO), the Employees’ State Insurance Corporation (ESIC), and the Income Tax Department. You still manage the work, culture, and deliverables; the EOR manages the taxes, registrations, and filings that keep your team compliant.

Here’s what that looks like in practice:

1. Registration with indian authorities

Every employee is registered under the EOR’s local entity for:

- EPFO – for Provident Fund compliance.

- ESIC – for social insurance coverage where applicable.

- Income Tax Department – for accurate TDS (Tax Deducted at Source) tracking.

This ensures all employees are legally recognized, tax-registered, and eligible for statutory benefits from day one.

2. Monthly payroll calculations and filings

Each month, your EOR:

- Calculates gross-to-net salary using current tax rates, exemptions, and allowances.

- Withholds TDS, PF, and ESI as required under Indian law.

- Remits contributions and taxes to the correct departments before the statutory deadlines.

- Files PF and ESI challans and Form 24Q (quarterly TDS return) accurately and on time.

These filings are not optional; missing even one can trigger penalties from the Income Tax Department or the Ministry of Labour.

3. Payslips, reporting, and end-of-year documents

Every employee receives a bilingual payslip (English + local language where required) showing itemized earnings, deductions, and employer contributions.

At the end of the financial year, the EOR also provides:

- Form 16 – for income tax reporting.

- PF/ESI statements – proof of social security compliance.

- Tax and compliance certificates – for employer records and audits.

This documentation keeps both your team and your business fully transparent to Indian authorities.

4. Complete compliance, one invoice

Instead of maintaining multiple registrations, filings, and remittance accounts, you get one monthly invoice from your EOR. It covers everything: salaries, taxes, contributions, filings, and administrative costs. You see a clean payroll summary; your EOR handles every form, challan, and filing behind the scenes.

Hiring in India doesn’t have to mean learning the tax code by heart.

Your team focuses on delivery, and your EOR ensures every rupee is filed where it should be.

Cost implications: The true price of compliance

Here’s what most companies discover too late: payroll compliance isn’t expensive; getting it wrong is.

Every global employer expanding into India faces the same question: do you build compliance in-house, outsource it to a local accountant, or use an Employer of Record (EOR)? On paper, all three options can handle payroll. In reality, only one gives you speed, predictability, and zero risk.

Let’s break down the cost and complexity behind each path.

Option 1: Setting up a local entity

The “traditional” route sounds appealing until you run the numbers.

Upfront setup costs:

- Company incorporation, legal, and translation fees: ₹75,000–₹150,000+

- EPFO, ESIC, and GST registrations

- Opening corporate bank accounts

- Hiring an accountant and payroll specialist

Monthly costs:

- Accounting and compliance retainers: ₹25,000–₹50,000+

- Payroll software, HR tools, and audit support

- Time (and stress) spent tracking state-level filings and tax changes

You gain control, but it comes with administrative drag and long-term liability; every misstep or delayed filing is on your books, not your consultant’s.

Option 2: Outsourcing to local accountants

Hiring a payroll bureau or accountant is cheaper in the short run but rarely clean in the long run.

Here’s why:

- Most small firms only manage TDS, not PF, ESI, or state-level filings.

- Data is often shared through spreadsheets and emails, not secure systems.

- You still remain the legal employer, which means you carry the compliance risk.

Average cost: ₹10,000–₹20,000/month, plus your internal time reviewing filings and coordinating with multiple agencies.

It looks affordable until a PF audit letter shows up.

Option 3: Using an Employer of Record (EOR)

This is where simplicity starts paying for itself.

With Team Up as your EOR in India, you don’t need a local entity, accountant, or HR staff on the ground.

You pay a flat monthly fee per employee (no percentage markup) that includes:

- Legal employment under TeamUp’s Indian entity

- Payroll calculation, tax deduction, and remittance

- EPFO, ESIC, and TDS filings

- Payslips, Form 16, and compliance reports

- Local benefits and HR admin

Global providers often charge 8–15% of salary as their EOR fee, meaning your cost grows with seniority.

Team Up’s flat-rate model keeps that fee predictable no matter how senior your hire is, so you can scale teams without hidden increases.

Realistically, you’ll spend about 25–30% less than managing your own entity, and gain complete compliance coverage in return.

What you’re really paying for

You’re not paying for payroll software. You’re paying for protection from fines, backdated taxes, and sleepless nights wondering if your filings went through.

With Team Up’s model, every rupee is accounted for, every return filed on time, and every team member legally covered under Indian labor law, all through one clean monthly invoice.

Final thoughts

Hiring in India opens doors to one of the world’s deepest, most diverse talent pools, but it also drops you into one of the most tightly regulated payroll systems in Asia.

Between TDS filings, EPFO registrations, ESI returns, and state-level professional taxes, even well-intentioned companies can find themselves tangled in red tape before their first hire’s payslip is printed.

That’s why global teams trust Team Up. We handle every part of payroll and compliance, registering your employees, managing taxes, and filing everything with the right authorities, so you can focus on growth, not government forms.

You get the people. We handle the paperwork. Everyone stays compliant.

Ready to hire in India without touching tax paperwork?

Schedule a call with Team Up and see how easy compliant hiring can be.

Frequently asked questions

What are payroll taxes in India?

Payroll taxes in India are the mandatory contributions and deductions made from an employee’s salary and the employer’s side payments to the government. These include income tax (TDS), Provident Fund (PF), Employees’ State Insurance (ESI), and Professional Tax (PT) in some states. When working with an Employer of Record (EOR), these payroll taxes are automatically calculated and filed in compliance with Indian labor and tax laws.

How are payroll taxes different from personal income taxes in India?

Payroll taxes and personal income taxes are related but not the same.

- Payroll taxes are deducted and paid by the employer on behalf of employees (like PF, ESI, and PT).

- Personal income tax is the employee’s direct tax on earnings, withheld as TDS (Tax Deducted at Source). An EOR in India ensures both sets of taxes are calculated, withheld, and filed correctly.

Which payroll taxes are paid by employers only in India?

Employers in India contribute to several mandatory schemes, including:

- Employer Provident Fund (EPF): 12% of employee salary (basic + DA)

- Employees’ State Insurance (ESI): 3.25% of gross salary (for eligible employees)

- Labor Welfare Fund (LWF): Employer contribution varies by state (₹3–₹25 per employee)

- Gratuity and Bonus Contributions: As per the Payment of Gratuity Act and Bonus Act, these costs are borne entirely by the employer and managed efficiently by an EOR provider.

How are payroll taxes calculated in India?

Payroll taxes are calculated based on gross salary components (basic pay, allowances, and bonuses) and statutory thresholds. For example:

- EPF = 12% of basic pay (employer and employee each contribute 12%)

- ESI = 0.75% (employee) + 3.25% (employer) if gross salary ≤ ₹21,000

- Professional Tax = ₹200/month (varies by state)

- TDS = According to the Income Tax Act, based on income slabs An EOR uses local payroll software to calculate these accurately every month.

What payroll taxes are paid by employers only in India?

Employers alone pay:

- Employer’s contribution to EPF (12%)

- Employer’s share of ESI (3.25%)

- Labor Welfare Fund (where applicable)

- Gratuity (4.81% of basic salary, accrued monthly) .These are not deducted from the employee’s salary—they’re additional costs covered by the employer.

How do I manually calculate payroll taxes for employees in India?

To manually calculate payroll taxes:

- Subtract employee PF (12%) and ESI (0.75%) from gross pay.

- Apply TDS based on annual income tax slab rates.

- Deduct Professional Tax (if applicable).

- The remaining amount is net take-home pay. For compliance, an EOR uses automated systems to avoid manual errors and ensure timely payments.

What are some examples of payroll taxes in India?

Examples include:

- Employer contributions: EPF, ESI, Labor Welfare Fund, Gratuity

- Employee deductions: EPF, ESI, TDS, and Professional Tax. Together, these make up the complete payroll tax structure that an EOR manages for both sides.

How are payroll taxes computed for international employees in India?

For foreign employees working in India, payroll taxes include income tax and applicable social contributions (EPF if they qualify as “international workers”). An EOR ensures all taxes are calculated in line with Double Tax Avoidance Agreements (DTAAs) and Indian residency rules.

How does an Employer of Record (EOR) simplify payroll tax compliance in India?

An EOR in India acts as your local legal employer, managing:

- Payroll calculations and filings

- Tax withholdings (TDS, PF, ESI, PT)

- Payments to government portals

- Employee payslips and statutory reports This eliminates the need for you to set up a local entity or handle complex regional regulations.

How to compute payroll taxes automatically using an EOR system?

EOR platforms use government-updated algorithms to calculate:

- Gross-to-net pay

- Employer and employee contributions

- Statutory deductions by state and salary band. This ensures real-time accuracy and compliance without manual intervention.

How do payroll taxes differ from income taxes for employers in India?

Payroll taxes are employer liabilities, while income tax is an employee liability. Employers fund statutory schemes like EPF and ESI, whereas income tax (TDS) is deducted from the employee’s earnings. An EOR keeps both aligned, ensuring there’s no underpayment or double taxation.

.svg)